🎰 Gambling Reform | Consumer Rights

A new app promises there is “no negative for anyone” in handing over real-time access to your entire financial life. British punters will forgive a degree of scepticism.

geoffbanks.bet · May 2026

There is a sentence in the GamScore press release that deserves to be read slowly, preferably while sitting down with a strong cup of tea. ☕

“There’s no negative for the regulator, the operator and the consumer. It’s a massive tick for all of them.”

No negative for anyone. Not one. A massive tick all round. I have not encountered language this comprehensively reassuring since the last time a bookmaker wrote to inform me that my account remained technically open but my maximum stake on British horse racing had been adjusted downward for operational reasons. No negative whatsoever. Massive tick. 👍

GamScore is a new consumer ‘wellbeing’ app launching in October 2026. It will use open banking to read your bank account three times a day. It will feed everything it finds into an algorithm that generates a personal risk score. (out of ten??) Your bookmaker will have access to that score. It will flag activity consistent with offshore or unlicensed betting and report aggregated intelligence about that activity to regulators. And it will do all of this, the company cheerfully announces, for free. 🆓

For free! Splendid. That settles it then.

“When someone in the gambling industry tells you there is no negative for the consumer, check your pockets. There is always a negative for punters. And I am a Bookie.”

🔍 What Open Banking Actually Means

Here is the thing about open banking that GamScore’s marketing materials glide past with considerable elegance. When you grant open banking access to a third party, they do not see only your gambling transactions. 🎯 They see your entire current account. Every debit. Every credit. The mortgage. The salary. The Tesco shop. The school fees. The Pornhub subscriptions. The VPN subscriptions (ties into Pornhub ecosystem) The private medical invoice. All of it. Labelled, dated, and now sitting on someone else’s servers. Somewhere.

GamScore says it is looking at your gambling behaviour. What it is actually receiving is a continuously updated picture of your entire financial life, refreshed three times a day. The gambling transactions are perhaps five lines out of five hundred on a typical monthly statement. GamScore gets all five hundred. 📊

That data, incidentally, is commercially extraordinary. Income verification. Spending patterns at merchant level. Debt signals. Payday correlations. The kind of information financial services firms spend serious money trying to infer. GamScore receives it directly, at no cost to itself, because you blithely handed it over in exchange for a dashboard, a score, and, let’s face it, a sporting Yankee. Lovely dashboard though, presumably. 💻

🕵️ The Privacy Policy That Forgot the Product

At this point you may be wondering what GamScore’s published privacy policy says about all of this data? Or maybe you just don’t care? 🤔

The privacy policy, published 1st May 2026 and generated using a free online tool called CookieYes, lists the personal information it collects. There are three items. Your name. Your email. Your mobile number.

That is it. 🫠

The open banking data does not appear. The transaction history is absent. The AI risk score is absent. The black market activity flags are absent. It is, as one commentator elegantly put it (and I am stealing it), the data protection equivalent of a surgeon’s consent form that mentions car parking but omits the surgery.

The policy does note that it may be revised “at any time without any prior notice,” with new terms taking effect 180 days after posting, and that your continued use of the app constitutes acceptance. So the rules governing what GamScore does with your bank account can change, unilaterally, without telling you, and your silence counts as agreement. British punters are, of course, broadly familiar with arrangements in which the rules change without warning and silence is treated as consent. We encounter it every time we try to place a bet at a reasonable stake. 🙃

🏴☠️ The Black Market Monitoring Twist

Here is the detail that deserves more attention than it has received. GamScore will not merely monitor your activity at licensed operators. It will identify “behavioural patterns consistent with unregulated betting” and provide “regulators with aggregated insights into market trends.”

Consider the population of British bettors currently using offshore operators. Many of them are there because they were driven there by document demands, account restrictions, and stake limits from licensed bookmakers. Having escaped one surveillance regime, they are now being offered a consumer ‘ ‘wellbeing’ app (bless them) that will identify their offshore activity and report it upstream to the same regulatory infrastructure that created the problem in the first place. 🔄

The app that promises to fix affordability checks will, as a design feature, flag the people who left because of affordability checks. There is a circularity here that should give everyone nightmares. 🤯

😍 A Regulator’s Wet Dream

Let us pause and consider who benefits most elegantly from this arrangement, because it is not the punter. 🎯

The Gambling Commission has spent years trying to build a comprehensive surveillance architecture around British bettors. It has faced parliamentary opposition, judicial review threats, accusations of acting ultra vires, a public petition signed by tens of thousands, and sustained pressure from the racing industry. Every step toward a mandated financial monitoring regime has come with a political and legal cost. GamScore solves all of that in one move. 🪄

Think about what the Commission gets here. It gets a single customer view of British bettors’ financial lives, updated continuously, without having to amend the LCCP. It gets black market intelligence it has never been able to gather systematically, fed to it as aggregated regulatory insight, without having to build the infrastructure itself. It gets a compliance lever over operator customer management without having to fight another consultation. And crucially, it gets all of this while maintaining perfect plausible deniability. The Commission did not mandate GamScore. Consumers chose it freely. The regulator merely expressed enthusiasm (exploded all over themselves) for innovative solutions and the market responded. 🙄

This is the dream of every regulator that has ever been frustrated by democratic accountability. Outsource the surveillance to a private company. Let consumers opt in voluntarily. Call it empowerment. Receive the data. The Gambling Commission has been trying to get a real-time view (peer up your crevice with a davy lamp) of bettor financial behaviour since at least 2020. GamScore proposes to hand it over, funded by consumers themselves, wrapped in a wellness dashboard and a personalised score. If the Commission endorses this, and the press release strongly implies it will, it will have achieved through a Swindon startup what six years of formal consultation could not deliver. The punter pays for his own monitoring. Everybody wins. Except, err, the punter. 🏇

💰 The “Free” Question Nobody Is Answering

GamScore Phase 1: consumer wellbeing app. Free. October 2026.

GamScore Phase 2: operator compliance tool. Sold to bookmakers. Early 2027. 💼

Within roughly three months of consumers downloading the free ‘wellbeing’ app and granting access to their bank accounts, GamScore monetises that infrastructure as a compliance product sold to the bookmakers those same consumers bet with. The consumer is not the customer. The consumer is the dataset. 📦

This is not a conspiracy theory. It is the stated business model, laid out in the press release in plain English. Phase 1 acquires the data. Phase 2 sells it. The only question is why nobody has asked about it more directly. Well, at least until contrarians like me came along

“The friction, it turns out, was the form-filling. The surveillance was always fine.”

🤝 The BHA’s Interesting Position

The BHA, which has spent several years vocally opposing affordability checks on the grounds that they are intrusive and treat ordinary bettors as suspected criminals, has described GamScore as “an interesting intervention.” Ok, thanks for playing. 🧐

🎮 How Operators Will Actually Use This

GamScore describes its Phase 2 product as a “single customer view.” That phrase deserves unpacking because it sounds fluffy and warm, and is neither. 🔬

British punters already know what operators do with information about their betting behaviour. They restrict your stakes. They close your account. They limit your markets. They do all of this unilaterally, without explanation, without appeal, and without any obligation to tell you what triggered the decision. The legal framework gives operators near total discretion over who they serve and on what terms. That has not changed. What GamScore changes is the quality and granularity of the information feeding those decisions. 📉

Currently an operator sees what you do on their platform. With GamScore’s single customer view, they see what you do everywhere. Your profit and loss across multiple accounts. Your betting frequency patterns across competitors. Your financial trajectory from your bank statement. Your chasing behaviour identified by an AI that updates three times daily. All of it processed, scored, and served up to the operator in a conveniently actionable format before you have even placed your morning bet. ☀️

And then what? The press release is silent on consequences, which is the most important silence. Because the BGC Code Handbook already requires operators to take action when indicators of harm are identified. GamScore, feeding into that framework as a Phase 2 compliance product, becomes the trigger mechanism for those actions. Your score drops because you had three consecutive losing days, or perhaps you just paid your wife’s Amex. The algorithm flags it. The operator’s compliance system receives the signal. Your account is restricted before you have spoken to anyone, appealed anything, or been given any opportunity to explain that you are a professional punter having a bad week. ❌

The operator does not have to justify this to you. They never have. They will not start now. What changes is that the decision will no longer even feel like a human one. It will arrive as an automated consequence of a number generated by an algorithm you did not design, running on data you provided under a wellness framing, governed by terms that can change without notice. The bookmaker who previously closed your account because you were winning will now close it because a score said so. Accountability has not improved. It has simply been outsourced to mathematics, which is considerably harder to argue with. 🤖

GamScore calls this empowerment. You own your score. It is on your dashboard. Your name is on the front. Which is rather like being told you own the rope they tied you with. 🪢

⚖️ The Verdict

geoffbanks.bet — Bottom Line

Let us be completely clear about what GamScore is, because the press release has worked hard to ensure you are not. 🎯

It is not a consumer protection product. A consumer protection product protects consumers from external threats. GamScore protects the industry from consumers, by building a continuously updated intelligence file on every bettor who signs up and distributing that file, in scored and processed form, to the operators those bettors use. The consumer is not the beneficiary. The consumer is the subject. 📋

It is not a privacy-respecting alternative to affordability checks. Its privacy policy was generated by a free online cookie tool, covers three data fields, omits the entire commercial foundation of the product, and reserves the right to change its terms without telling you. A product proposing to hold real-time access to millions of British bank accounts has less published data governance than a local dentist’s appointment booking system. 🦷

It is not free. Nothing that costs this much to build and operate is free. What is free is the consumer acquisition. The monetisation is the Phase 2 operator compliance product, sold to bookmakers using the data consumers handed over for nothing in Phase 1. 📦

It is not independent. It has positioned itself explicitly as the answer to a Gambling Commission call for innovative solutions, which means it is angling for regulatory endorsement from day one. An entity that needs the regulator’s blessing to succeed is not going to challenge the regulator’s priorities. It is going to serve them. 🫡

And it will not reduce the black market. Bettors driven offshore by intrusive checks and unilateral account restrictions will not return to a licensed market that now monitors their bank accounts three times a day, scores their behaviour algorithmically, flags their offshore activity to regulators, and feeds all of it to the operators who already restricted their stakes. They will stay offshore. They will tell their friends. The black market does not shrink when the licensed market is put under a commercial microscope. It grows. 📈

The Gambling Commission spent six years and considerable political capital trying to build a financial monitoring regime for British bettors. GamScore proposes to hand them something far more powerful, funded by the bettors themselves, with a wellness logo on the front. If the Commission endorses it, they will have confirmed what critics have argued for years. That this was never about harm reduction. It was always about control. 🔒

There is no negative for anyone, Josh Apiafi tells us. The punter begs to differ. The punter, as usual, wasn’t really part of the conversation. 🏇

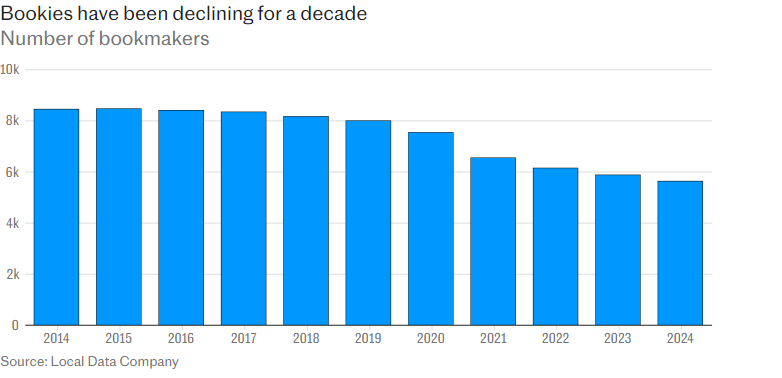

However, three long-term consumer demand trends are much more sticky than channel shift.

However, three long-term consumer demand trends are much more sticky than channel shift. The relative growth in slots has therefore partially mitigated the relative decline of National Lottery revenue to keep gambling expenditure as a proportion of Household Disposable Income relatively stable at c. 1% over 25 years (note, FY9 was low because of the implementation of the Smoking Ban, the loss of S16/21 machines, and the onset of a global recession). However, an underlying decline can be detected and if the National Lottery is not turned around then it is likely to become more visible, in our view.

The relative growth in slots has therefore partially mitigated the relative decline of National Lottery revenue to keep gambling expenditure as a proportion of Household Disposable Income relatively stable at c. 1% over 25 years (note, FY9 was low because of the implementation of the Smoking Ban, the loss of S16/21 machines, and the onset of a global recession). However, an underlying decline can be detected and if the National Lottery is not turned around then it is likely to become more visible, in our view. For all the hype about a changing landscape, very little is changing in terms of underlying consumer behaviour other than channel shift. British consumers are, if anything, gambling less, albeit with revenue concentrated in a smaller number of participants.

For all the hype about a changing landscape, very little is changing in terms of underlying consumer behaviour other than channel shift. British consumers are, if anything, gambling less, albeit with revenue concentrated in a smaller number of participants.