HOW THE GAMBLING COMMISSION IS FAILING PUNTERS AND RACING

Betting & Regulation

The Right to Bet:

How the Gambling Commission Is Failing Punters, Racing and the Law

Affordability checks are being imposed on millions of ordinary bettors on the basis of flawed evidence, without legal authority, and with consequences the regulator either cannot see or chooses to ignore. It is time to say so plainly.

Gambling is legal in Great Britain. It has been freely permitted, and indeed actively liberalised, since the Gambling Act 2005 created one of the most open betting markets in the world. The legislation that established this framework also created the Gambling Commission, and it imposed on that body a clear statutory duty: not merely to pursue the licensing objectives of protecting the vulnerable and preventing crime, but to permit gambling, in so far as the Commission thinks it reasonably consistent with those objectives.

That duty is not decorative. It is not a footnote. It sits in section 22 of the Act alongside the harm-prevention objectives, carrying equal legal weight. The Commission was never intended to be a body that restricts gambling whenever it can find a rationale — it was intended to be a regulator that allows a lawful activity to flourish while managing genuine risks. By any honest assessment, it has drifted very far from that mandate.

The “Choice” That Is No Choice at All

In a recent smartbetting podcast interview, Gambling Commission chief executive Andrew Rhodes was confronted with a direct and reasonable question. Punters are currently being told by bookmakers — among them bet365, one of the largest operators in the world — that if they wish to continue betting at certain levels, they must enrol in an open banking service called Bet Budget and grant access to their financial records. In some cases, we are told, this means sharing five years of complete bank account history across all accounts held.

The interviewer put this squarely to Rhodes: is this really a choice? Rhodes replied that it is a consumer choice — they decide whether or not to use open banking. The Commission is not doing this. The operator is doing this. And if you don’t like it, you can choose not to.

This answer deserves to be examined carefully, because it is not an honest account of what is happening.

The exchange — verbatim

“Their choice is adhere to this or you can’t bet with us — so it’s not really a choice, is it?”

— Interviewer, Smart Betting Club Podcast

“It’s a choice as in you can bet or you can’t.”

— Andrew Rhodes, Gambling Commission CEO

That response — “you can bet or you can’t” — is, in effect, an endorsement of coercion dressed up as consumer autonomy. The logic, applied consistently, would justify almost any operator imposition. A bookmaker could demand you provide your passport, your payslips, your mortgage documents and a letter from your employer, and the regulator’s position would be: that’s the operator’s commercial decision, and you are free not to use them. This is not consumer protection. It is the abandonment of it.

What makes it worse is that the Commission has spent years applying regulatory pressure — through enforcement reports, compliance activity, and implied threat of licence sanction — that has driven operators toward exactly this behaviour. The checks that Rhodes presents as “operator choices” are, in very large part, a direct consequence of Commission pressure applied through channels that were never subjected to formal rule-making or parliamentary scrutiny. Operators did not suddenly decide, of their own commercial volition, that demanding five years of bank records from punters was good for business. They did it because they were afraid of what would happen if they didn’t.

The Legal Duty Being Ignored

Section 22 of the Gambling Act requires the Commission to aim to permit gambling. This is not a vague aspiration. It is a positive obligation, and one that has meaningful content. The “reasonably consistent” qualifier that follows it requires the Commission to balance the duty to permit against the licensing objectives — it does not allow harm prevention to operate as an absolute trump card that extinguishes all other considerations.

Consider what proportionality requires in this context. The enforcement cases that provided the Commission’s original justification for pushing operators toward affordability checks involved genuinely extreme conduct: people losing hundreds of thousands of pounds without any check whatsoever, operators treating clearly distressed customers as VIPs. Nobody defends that. Nobody should.

But the regulatory response has not been calibrated to address those extreme cases. It has been applied at a level so far below them that it now routinely catches ordinary recreational punters — people losing a few hundred pounds a month on horse racing, betting within their means, causing harm to nobody — and subjects them to intrusive interrogation about their personal finances. The Commission’s own proposed thresholds would trigger checks at net losses as low as £150 in a month. At one point in the debate, the figure of £1.37 a day was cited as the effective threshold for frictionless financial vulnerability checks. The Commission did not dispute this arithmetic.

It is very difficult to argue that a policy causing documented, serious collateral harm — to a lawful industry, to hundreds of thousands of ordinary consumers, to the financial ecosystem of British horse racing — while failing to demonstrate any measurable reduction in problem gambling rates, satisfies the proportionality test that section 22 implicitly requires.

The “3%” That Tells a Misleading Story

Throughout this debate, the Commission and government have repeatedly invoked the figure that only 3% of accounts will be affected by enhanced financial risk checks. This has been treated as a reassurance — a signal that the vast majority of punters have nothing to worry about.

It is not an honest reassurance. It is a number that has been selected, presented and sustained in its most politically convenient form.

The 3.2% figure comes from a survey of 5.86 million active accounts covering May 2020 to April 2021. It represents the proportion of accounts losing £2,000 in a rolling 90-day period in a single year, at 2020 price levels. From that baseline, the problems compound quickly.

The thresholds were never inflation-adjusted before implementation. By summer 2024, when the policy was due to begin, £2,000 at 2020 prices had risen to approximately £2,528 in real terms. The figures simply weren’t updated. On inflation-adjusted terms, around 4.1% of accounts would breach the 90-day threshold, and 2.5% would hit the 24-hour £1,000 threshold. Because accounts can qualify for both, the true affected proportion is higher still — the Commission’s own analysis confirmed that between a fifth and a quarter of individuals identified by one threshold did not exceed the other, meaning the number of unique individuals affected is notably higher than either figure alone suggests.

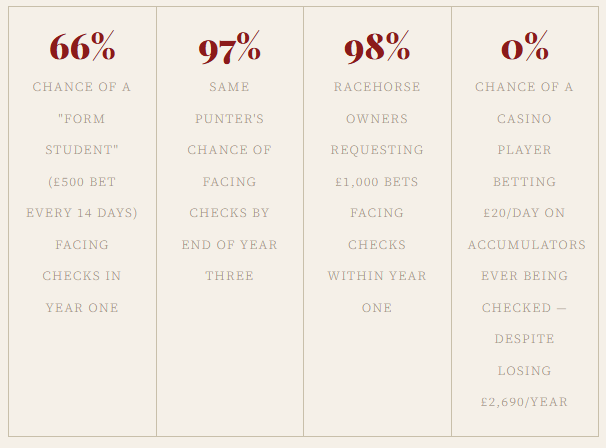

More importantly, 3% in year one is not 3% in year three. The process is not stationary. Accounts that avoid checks in year one can breach a threshold in subsequent years as results accumulate. Independent simulation modelling of typical racing punter profiles makes this vivid:

That last figure deserves emphasis. The threshold design is structurally biased. A punter placing modest daily accumulator bets at a high operator margin — losing nearly £2,700 a year — will never trigger a check, because steady daily losses don’t produce the variance spikes that trip the thresholds. Meanwhile a knowledgeable racing punter placing a single £500 fortnightly wager will almost certainly face checks within three years, even if they are profitable overall.

The policy, in short, disproportionately targets the most engaged, most informed, most economically valuable customers of horse racing — while largely ignoring the steady, high-frequency, low-unit gamblers that arguably represent a greater harm risk. This is not a technicality. It is a fundamental design failure that the Commission has never adequately addressed.

Horse Racing: Not Collateral Damage. A Foreseeable Catastrophe.

When the podcast interviewer asked whether the knock-on effect on sports like horse racing was “just collateral damage”, Rhodes demurred. He acknowledged racing’s unique dependency on gambling — 70% of its gross gambling yield comes from just 1% of accounts, five times the concentration of other sports. He acknowledged a declining consumer base. He then suggested that racing has structural problems independent of affordability checks and that it’s “not really for the Gambling Commission to comment on the economics of horse racing.”

This position is not sustainable. The Commission’s regulatory decisions are a direct, proximate, and now quantified cause of racing’s financial deterioration. The claim that this is somehow outside the Commission’s remit is precisely the kind of institutional detachment from consequences that makes this situation so frustrating.

“The Gambling Commission increasingly appears to be unaccountable and out of control. Moreover, they continue to be unable to demonstrate any evidence as to the impact that the current affordability measures are having on problem gambling rates.”— Martin Cruddace, CEO, Arena Racing Company

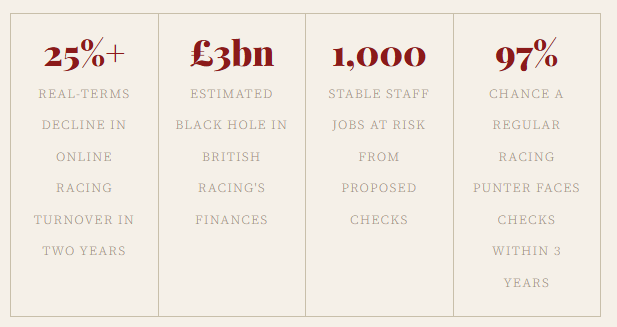

The numbers are not in dispute. Online racing turnover fell to £8.37 billion in the year to March 2024, compared to around £10 billion two years previously. Had it grown in line with inflation, it would be close to £11.5 billion — a real-terms decline of more than 25%, or a gap of some £3 billion. The BHA’s own data shows turnover year-to-date at end of August 2024 was down a further 9.5%, suggesting the decline is accelerating rather than stabilising.

The levy that funds racing’s prize money, its safety infrastructure, its veterinary research — all of it flows from betting turnover. British racing already receives less than 3% of betting revenue, compared to 7.7% in France and 8.4% in Ireland. It cannot absorb a 25% revenue shock. The mathematics are not complex.

Independent economic modelling by Regulus Partners, commissioned by the BHA, estimated that up to 1,000 stable staff jobs — one in seven — could be lost if the current proposals are implemented in full. These are not executive positions. They are the people who care for 14,000 thoroughbreds in training, who work in rural economies across Britain, who are not rich and who have no obvious alternative employment in the areas where racing yards operate.

“Racing cannot take any more financial setbacks. Racing and betting have come together on this issue like never before, because they know that they face the greatest ever threat to their existence.”— MP Philip Davies, Westminster Hall debate, February 2024

British racing contributes £4.1 billion to the British economy. It employs 80,000 people directly and 100,000 indirectly. It supports 8,000 small and medium enterprises. It touches 60 marginal parliamentary constituencies. It is not a fringe activity of the wealthy. It is a rural industry, deeply embedded in British cultural and economic life, and it is being hollowed out by a regulator that cannot demonstrate that what it is doing is working.

The Black Market: The Risk the Commission Keeps Minimising

Perhaps the most concerning aspect of the Commission’s posture throughout this period has been its persistent tendency to underweight the black market risk. At a Culture, Media and Sport select committee hearing, Rhodes said that every time he had heard someone say people were going to the black market, he had asked them where, and had never received an answer he could act on. This was presented as scepticism about the phenomenon’s scale.

Since then, Yield Sec data has shown a substantial increase in black market gambling, with visits to unregulated sites from UK users tripling during the 2022 World Cup, with peaks during Cheltenham and Royal Ascot — precisely the events most associated with the racing audience being disrupted by affordability checks. Rhodes contested the methodology. He may have points. But the direction of travel is not seriously in dispute, and his earlier scepticism now looks like something he has had to quietly retreat from.

What no one in the Commission’s leadership has grappled with honestly is the fundamental policy logic problem. If affordability checks in the regulated market drive even a fraction of consumers to the unregulated black market, the harm-prevention case for those checks collapses. Black market operators have no safer gambling tools, no self-exclusion obligations, no consumer protections whatsoever. They don’t want winning punters, and they are notorious for not paying out. A policy that displaces people from a regulated environment into that landscape has made those consumers worse off by every measure the Commission claims to care about.

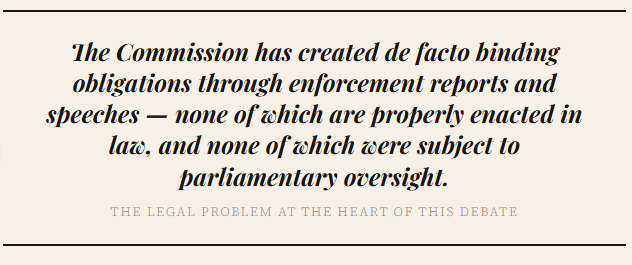

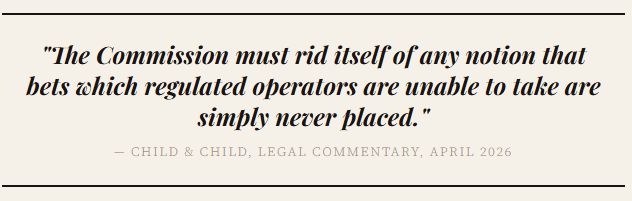

The Commission appears to operate on an implicit assumption that bets which regulated operators are unable to take simply will not be placed. That assumption is not credible. It never was.

What Honest Accountability Looks Like

None of this is to argue that gambling requires no regulation, or that every punter is responsible and every operator trustworthy. The cases that prompted government action — people losing hundreds of thousands without any interaction from the operator — were genuinely indefensible. The regulatory impulse behind affordability checks is not unreasonable in origin.

But reasonable in origin does not mean appropriate in execution. And the Commission has failed, repeatedly and seriously, on execution:

It applied regulatory pressure through enforcement reports and informal guidance without formal rule-making, creating binding practical obligations that were never subjected to legal scrutiny or parliamentary oversight. It allowed years of chaotic, inconsistent, operator-by-operator affordability checking to cause real harm to real consumers before attempting to standardise anything. It cited a “3% of accounts” figure that was stale, not inflation-adjusted, accounts-not-people, and systematically selected to understate real-world exposure. It pushed a pilot scheme to test whether frictionless checks work — after those checks had already been de facto implemented and had already caused the damage the pilot was supposedly designed to prevent. It has been unable, after years of this regime, to point to any evidence that problem gambling rates have fallen as a result. And it has watched a 25% real-terms collapse in horse racing turnover — a lawful industry it is legally obliged to permit — and described it as something it cannot properly comment on.

That is not the record of a regulator carrying out its statutory duty. It is the record of a body that has allowed one interpretation of one part of its mandate to crowd out everything else, without accountability and without evidence that the approach is working.

What Needs to Happen

The government should require the Gambling Commission to publish, before any formal implementation of enhanced financial risk checks, a full impact assessment that quantifies: the reduction in problem gambling rates attributable to current affordability measures; the proportion of consumers displaced to the unregulated market as a result; and the economic damage to horse racing and the wider rural economy. If such an assessment cannot be produced — because the evidence does not exist — then the policy cannot be justified.

The Commission should acknowledge formally, and in its regulatory guidance, that it has a statutory duty to permit gambling, and that this duty imposes a proportionality requirement on everything it does. The harm-prevention licensing objective does not override that duty. It must be balanced against it.

The open banking situation — where consumers are told by regulated operators that they must surrender five years of complete financial data or be refused service — must be directly addressed. Rhodes’ characterisation of this as a “consumer choice” is not acceptable from a regulator that is supposed to ensure gambling is fair and open. It is not open to say to a consumer: hand over your most sensitive personal financial information, or we won’t take your bet. That is not consumer autonomy. It is coercion, and the Commission should say so.

And the racing industry — which operates under a unique statutory funding relationship with the gambling sector through the levy — deserves specific recognition of the disproportionate impact that demand-side restrictions on betting turnover have on its finances. The Gambling Commission’s mandate to permit gambling is especially acute here: if it is permitting the regulated industry to collapse the consumer base for the very betting activity that funds an entire sport, it is not fulfilling its obligations under the Act.

Over 400 leading figures in racing — trainers, owners, jockeys, MPs of all parties — have signed an open letter to the Secretary of State calling for affordability checks to be scrapped. The BHA has warned that the Commission appears to be considering the pilot results without adequate government scrutiny of the consequences. Racing’s turnover is still falling.

The Gambling Commission was created to balance protection with permission. Right now, it is failing at both: it cannot demonstrate the protection is working, and it is presiding over the systematic destruction of a legal, economically vital industry it was legally obliged to protect. That is a regulatory failure of the first order, and it requires a direct political response — not more pilots, not more consultations, not more expressions of good intent.

British punters have a right to bet without being subjected to financial interrogation. British racing has a right to the regulatory environment the law promised it. Neither right is currently being honoured.

This analysis draws on the Gambling Act 2005, the Gambling Commission’s consultation responses and enforcement reports, parliamentary debate records (Hansard, February 2024), independent economic modelling by Regulus Partners, research published by the British Horseracing Authority, the Smart Betting Club podcast interview with Andrew Rhodes, legal commentary by Child & Child, and impact assessments published by gamblingreform.co.uk. All statistics are sourced from publicly available official data or named independent research.

Geoff Banks

CEO Geoff Banks Online

April 2026

However, three long-term consumer demand trends are much more sticky than channel shift.

However, three long-term consumer demand trends are much more sticky than channel shift. The relative growth in slots has therefore partially mitigated the relative decline of National Lottery revenue to keep gambling expenditure as a proportion of Household Disposable Income relatively stable at c. 1% over 25 years (note, FY9 was low because of the implementation of the Smoking Ban, the loss of S16/21 machines, and the onset of a global recession). However, an underlying decline can be detected and if the National Lottery is not turned around then it is likely to become more visible, in our view.

The relative growth in slots has therefore partially mitigated the relative decline of National Lottery revenue to keep gambling expenditure as a proportion of Household Disposable Income relatively stable at c. 1% over 25 years (note, FY9 was low because of the implementation of the Smoking Ban, the loss of S16/21 machines, and the onset of a global recession). However, an underlying decline can be detected and if the National Lottery is not turned around then it is likely to become more visible, in our view. For all the hype about a changing landscape, very little is changing in terms of underlying consumer behaviour other than channel shift. British consumers are, if anything, gambling less, albeit with revenue concentrated in a smaller number of participants.

For all the hype about a changing landscape, very little is changing in terms of underlying consumer behaviour other than channel shift. British consumers are, if anything, gambling less, albeit with revenue concentrated in a smaller number of participants.