Posted by Geoff Banks | geoffbanks.bet

Somewhere in a Birmingham office, a group of unelected bureaucrats are preparing to vote on whether to impose Financial Risk Assessments on British punters. No parliamentary mandate. No independent scrutiny. No published final pilot report. Just a Board nodding through what they spent six years lobbying for. 🙄

I know. Shocking.

Let’s set the scene. The Gambling Commission’s previous CEO, Andrew Rhodes, departed on 30 April 2026. His replacement as Acting CEO? Step forward Sarah Gardner. The same Sarah Gardner who once told a Danish regulator that she simply cannot accept the argument that driving customers off the regulated market and into illegal alternatives should slow down the Commission’s regulatory ambitions. Cannot accept it. Just won’t have it. 🚫

So the person who has declared black market growth an irrelevance is now running the organisation about to greenlight the policy most likely to cause it. Wonderful. Truly wonderful.

The Math That Isn’t Adding Up 🔢

The Commission’s Director of Major Policy Projects, Helen Rhodes, published a blog in April 2026 reassuring us that only “less than 3% of active customer accounts” would trigger any steps under the FRA proposals, and that 97% of those assessments would be completely frictionless.

Let us pause here and appreciate the artistry.

Three percent of accounts sounds tiny. A rounding error. A statistical footnote. Except the UK has roughly 22 million active betting accounts. Three percent of that is 660,000 people. 660,000 people who will, in the GC’s own framing, have their credit file silently interrogated by a third party data provider without their knowledge or consent, with no appeal mechanism, and with the operator obliged to act on whatever the algorithm spits out.

“Frictionless” for whom, exactly? 🤔

And remember: these are accounts, not people. Many regular punters hold accounts with multiple operators. The same individual triggers the check five times over. The 3% figure is not a measure of consumer impact. It is a number designed to sound reassuring in a press release.

The People Being Targeted Are Not the Problem 🏇💷

Here is the part the Commission really does not want you to think about too carefully. Because when you do, the entire FRA architecture collapses.

The 3% of accounts facing the heaviest scrutiny under FRAs are, by definition, the highest staking customers in the regulated market. These are not, in the main, problem gamblers. They are the economic engine of British horse racing and of the licensed betting industry as a whole.

Dan Waugh of Regulus Partners put it plainly: the problem gambling rate for people who bet on sport online is, in his words, “microscopic” unless those customers are also engaged in online casino products. Horse racing specifically has a lower problem gambling rate within sports betting than almost any other category. 📉

So who does suffer gambling harm at meaningful rates? The evidence consistently points not to the high rolling racing punter sitting in the Members at Goodwood, but to lower income individuals engaged in high margin, high frequency products. Online slots. Fixed odds terminals. Products with house edges of 4%, 10%, 40%. Products where consistent, predictable losses grind down people with less financial resilience. The GSGB data shows that problem gambling prevalence is modestly higher in lower income groups. The open banking studies the Commission itself commissioned showed that, interestingly, the most financially concerning gamblers had income levels around 21% above the average. Higher stakers tend to be higher earners. That is not a surprise. It is arithmetic. 💡

Yet the FRA architecture is calibrated to trigger on spend volume, not on product type, not on income ratio, not on any actual indicator of distress. And spend volume is exactly where the racing punter lives.

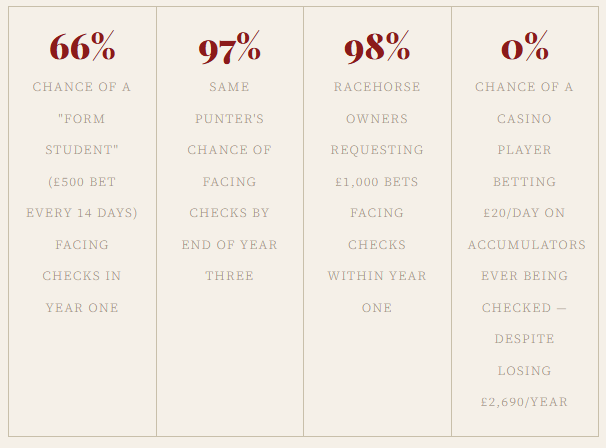

SharpBetting’s modelling of different customer types under the EFRC regime tells the story with brutal precision. A roulette player placing hundreds of small bets per day at a 2.7% house edge loses around £5,000 a year. They are almost never triggered for a check. After five years, only 2% of simulated roulette accounts faced an EFRC. An acca punter betting £20 a day on long shot multiples loses £2,690 a year on average. Never triggered once. Not a single check.

Meanwhile a Racing Enthusiast placing £25 bets on two selections a day at 8/1 loses around £1,800 a year. That is less than either the roulette player or the acca punter. Yet 76% of Racing Enthusiast accounts are triggered for a check by year three. A Form Student placing a single careful £500 bet every fortnight on a studied selection loses around £250 a year. 97% of Form Student accounts face a check by year three. She loses the least. She gets checked the most. 🤦

This is not a consumer protection regime. This is a system that identifies and interrogates the customers who bet intelligently on horse racing while waving through the customers who lose more money on online casino games. It is as if the policy were specifically designed to cause maximum disruption to the sport and product with the lowest harm profile in the entire regulated market. 🎯

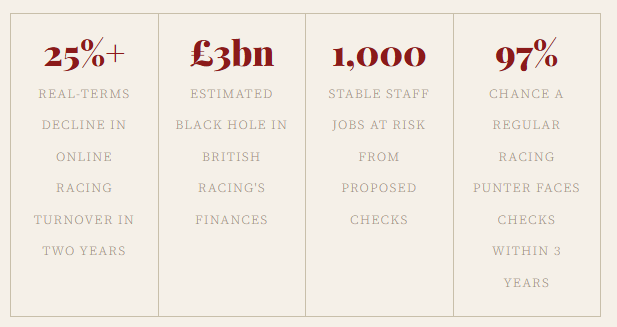

And the economic consequences of targeting precisely this cohort are devastating. Horse racing receives the Horserace Betting Levy, which last year generated £108 million. That sounds significant. But it is only a fraction of the total. When media rights, sponsorship, marketing and promotional activity funded by betting operators is included, higher staking customers contribute close to six times the value of the Levy back into the sport. We are talking about an economic relationship worth hundreds of millions of pounds to an industry employing tens of thousands of people, sustaining racecourses from Carlisle to Cheltenham, and underpinning the livelihoods of stable staff, trainers, jockeys, vets, bloodstock agents and everyone else in the ecosystem. 🏟️

The Racing Post’s Big Punting Survey found that among those regularly staking £500 or more, more than 50% had already been subjected to affordability checks. Not 3%. More than half. These are the customers on whom racing’s financial survival depends. One in five of those betting at £100 a time has already used a black market bookmaker in the last twelve months. More than one in three of those betting at £1,000 or more per bet has done so. They are not leaving the market because they cannot afford to bet. They are leaving because they are being treated like suspects while the regulator focuses its ideological firepower on the wrong product, the wrong customer, and the wrong type of harm entirely. 🚨

The Commission wants you to believe FRAs are about protecting the vulnerable. The evidence says they are systematically harassing the financially robust while doing next to nothing for the genuinely at risk. It is the regulatory equivalent of conducting drug searches at the golf club while waving through the inner city. And the sport that pays the price is the one that had the lowest harm rate to begin with.

The Commission vs The Commission 🥊

Here is where it gets genuinely funny. If you enjoy regulatory self-contradiction as entertainment, which you absolutely should.

The GC’s Compliance and Enforcement Report for 2019 to 2020 stated, in black and white, that customers wishing to spend more than the national average should be asked to provide payslips, P60s, tax returns or bank statements. Operators were told this was what compliance looked like. Fines followed for those who failed to implement it.

Fast forward to April 2026. Tim Miller, the Commission’s Executive Director, told the Ethical Gambling Forum that in 2026 it cannot be right that regulatory compliance still leads to some operators asking consumers to share financial documentation.

So operators were fined for not asking for documents. And now the Commission is appalled that operators are asking for documents.

The Commission spent four years training bookmakers to demand your payslips, and is now standing in front of a camera looking baffled that bookmakers are demanding your payslips. It is the regulatory equivalent of arson followed by a vigorous public statement condemning fire. 🔥🔥🔥

The Pilot Nobody Reviewed 🕵️

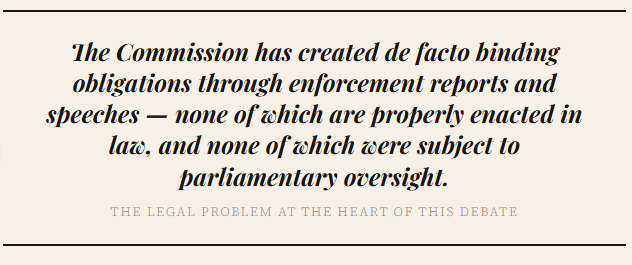

The entire justification for the Board vote rests on the FRA pilot. A pilot that concluded in summer 2025. A pilot for which no final, published, independent evaluation has been made available to the public, to Parliament, or to the industry.

Helen Rhodes’ April 2026 blog was described as an “update on post pilot analysis.” It was a Commission blog post. Written by a Commission employee. Reviewed by the Commission. Published on the Commission website to inform a Commission Board decision.

Dan Waugh of Regulus Partners put it well: the Commission cannot be allowed to mark its own homework, particularly when the dog has a habit of chewing inconvenient facts out of any assessment it undertakes.

No independent review. No OSR sign off. No parliamentary debate. No published data. Just a blog.

This is the evidence base on which they are voting. Take that in. 🤦

408 People Who Know More Than You Do 📢

Over 400 of the most senior figures in British horse racing, including trainers, owners, racecourse executives, and industry veterans, signed an open letter to Culture Secretary Lisa Nandy warning of the catastrophic consequences of FRA implementation. The BHA chief executive warned publicly that the government was sleepwalking into disaster. The Racing Post ran weeks of frontpage coverage detailing consumer harm, black market growth, and the chill on racecourse betting rings.

The Commission’s response? “Much of it has been ill informed or inaccurate.”

Yes. John Gosden: ill informed. The BHA board: inaccurate. 408 signatories representing billions in economic activity: not quite up to speed.

Meanwhile the Commission, whose leadership has no professional background in racing or betting, and which derives much of its ideological scaffolding from public health academics funded by a California based anti gambling billionaire, is, apparently, the voice of reason in this debate. 🎓💰

The Black Market Elephant 🐘

The Racing Post has reported that black market betting now accounts for an estimated 20% of UK racing turnover. William Hill owner Evoke has cited black market penetration as a factor in its UK revenue decline. Multiple senior racing figures have publicly admitted to betting on unregulated sites because they cannot get a bet on in the licensed market.

Sarah Gardner, the new Acting CEO, cannot accept this argument.

The unlicensed operators she cannot be bothered to worry about do not verify age. They do not contribute to the Horserace Betting Levy. They do not fund GamStop. They have no safer gambling obligations whatsoever. They take from the sport and give nothing back. And they are growing precisely because the regulated market is being made progressively more hostile to anyone who wants to have a proper bet.

But sure. Let’s vote to make the regulated market even less accessible. That will definitely fix the problem. 🤡

What Happens Next 📅

The Board votes. FRAs go through. Operators implement. The 3% that becomes 660,000 accounts gets their credit files silently checked. A meaningful proportion of those have insufficient credit data, or flags from financial difficulties unrelated to gambling, or simply do not match the threshold. Their operators are obliged to interact with them. Some will comply with whatever is asked. Many will not. They will close their accounts and open new ones on unlicensed sites based in Curaçao or Gibraltar or nowhere at all.

The Racing Post will write about it. The Commission will say the coverage is ill informed.

The Levy will fall. Racecourses will struggle. Small yards will close. Rural jobs will go.

The Commission will convene a working group to study the issue. They will publish an update blog. It will be written by a Commission employee, reviewed by the Commission, and published on the Commission website.

And somewhere, a Curacao sportsbook will be counting its new British customers and wondering what all the fuss is about. 💻🌴

The Gambling Commission is not a public health body. It is not a Treasury department. It is a licensing authority with a statutory duty under s.22 of the Gambling Act 2005 to aim to permit gambling. That duty has not been repealed. It is simply being ignored.

Vote against it. Write to your MP. Tell the BHA. Tell the BGC. Make some noise.

Because the Commission is about to make a decision it cannot be held accountable for, using evidence it will not publish, on behalf of consumers it does not represent, with consequences it refuses to acknowledge.

And nobody is stopping them. 🚨

Geoff Banks is a licensed remote betting operator. Views expressed are his own.

However, three long-term consumer demand trends are much more sticky than channel shift.

However, three long-term consumer demand trends are much more sticky than channel shift. The relative growth in slots has therefore partially mitigated the relative decline of National Lottery revenue to keep gambling expenditure as a proportion of Household Disposable Income relatively stable at c. 1% over 25 years (note, FY9 was low because of the implementation of the Smoking Ban, the loss of S16/21 machines, and the onset of a global recession). However, an underlying decline can be detected and if the National Lottery is not turned around then it is likely to become more visible, in our view.

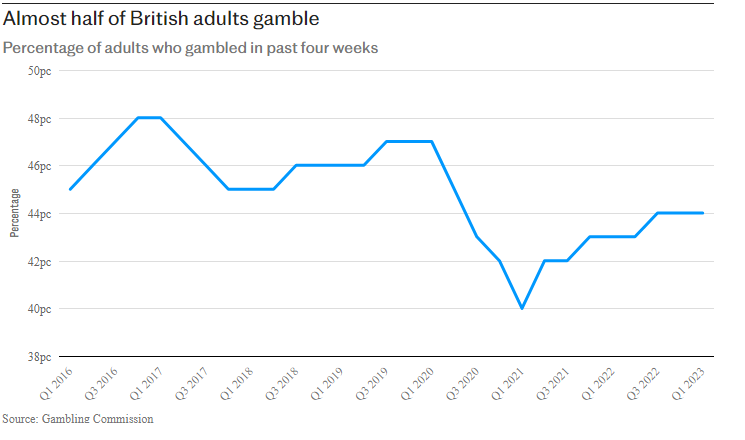

The relative growth in slots has therefore partially mitigated the relative decline of National Lottery revenue to keep gambling expenditure as a proportion of Household Disposable Income relatively stable at c. 1% over 25 years (note, FY9 was low because of the implementation of the Smoking Ban, the loss of S16/21 machines, and the onset of a global recession). However, an underlying decline can be detected and if the National Lottery is not turned around then it is likely to become more visible, in our view. For all the hype about a changing landscape, very little is changing in terms of underlying consumer behaviour other than channel shift. British consumers are, if anything, gambling less, albeit with revenue concentrated in a smaller number of participants.

For all the hype about a changing landscape, very little is changing in terms of underlying consumer behaviour other than channel shift. British consumers are, if anything, gambling less, albeit with revenue concentrated in a smaller number of participants.