Last year, the Gambling Commission wrote to the Betting and Gaming Council (‘BGC’) to ask it to stop referring to Health Survey statistics. It now transpires that it did so on behalf of the activist organisation, Gambling with Lives (‘GwL’)

Great Britain: Politics – is something rotten in the state of the West Midlands? A novel solution to addressing ‘problem gambling’ was briefly glimpsed in parliamentary debate last week – the imposition of strict gambling controls on people in the West Midlands; leaving those living elsewhere in England to flutter as they see fit.

During Wednesday’s Westminster Hall Debate on Gambling Harms, Sarah Coombes MP (Lab, West Bromwich) claimed that there were “168,000 people in the west midlands who say that problem gambling is devastatingly affecting their lives” and the lives of family members. Seconds earlier, Ms Coombes’s colleague, Jim Dickson MP (Lab, Dartmouth) had told the chamber, with the authority of the now defunct Public Health England (‘PHE’), that an identical number of people in the whole of England were experiencing ‘problem gambling’. Taken together, these statements appear to indicate that gambling may only be a problem for people living in the environs of Wolverhampton, West Bromwich, Walsall, Coventry and Birmingham (home of Britain’s Gambling Commission).

No sooner did this regional lockdown ‘public health approach to problem gambling’ hove into view, than it started to dissolve under the weight of wider MP interventions. Dawn Butler MP (Lab, Brent) argued that there are around 20,000 ‘problem gamblers’ in her constituency alone; and Cameron Thomas MP (LibDem, Tewkesbury) claimed (incorrectly) that PHE had put the national figure at 246,000. Other MPs insisted that there were in fact 1.3 million or more ‘problem gamblers’ in Great Britain – claims that rely on the misuse of official statistics, as defined by the Gambling Commission.

In general, the debate was a poor advertisement for parliamentary discourse. One Liberal Democrat MP suggested that supporters of Liverpool FC would find themselves “unable to talk to their friends and family about the losses and their addiction” as a direct result of Ladbrokes becoming the club’s official betting partner; while Butler of Brent claimed, without providing a shred of evidence, that gambling was “more addictive than heroin”. According to National Health Survey (‘NHS’) estimates, the rate of DSM-IV gambling disorder lies between 0.1% and 0.2% of the adult population, compared with 3.1% of people showing signs of drug dependency and a similar proportion with mild or severe alcohol dependency). As flies to wanton boys are statistics to MPs; they use them for their sport.

Only one participant – Labour’s Jake Richards, Member for Rother Valley – appeared to notice what was going on, observing that, “we have heard a lot of statistics in this debate, but they vary because we just do not know what we are dealing with”. Mr Richards was half-correct in his diagnosis. The real reason for the confusion is that prevalence rates are based on responses to self-report surveys – and estimates vary significantly depending on how these are conducted. NHS Health Surveys have historically been conducted in-person, an approach considered to be the “gold standard” in terms of yielding accurate results (Sturgis & Kuha, 2022). The Gambling Commission’s Gambling Survey for Great Britain (‘GSGB’) is conducted online and is less likely to be reliable due to low response rates and topic salience bias (ibid.). GambleAware’s Annual Treatment Survey uses self-selected online panels (surveys of people who actively choose to spend their time filling out questionnaires) and, while these panels may have their uses, providing reliable population-level figures is not one of them.

The chief executive of the Gambling Commission, Andrew Rhodes recently lamented that arguments over which survey is more accurate distract from what really matters. He is correct – but this is a situation of the Commission’s own making. Repeated attempts by the regulator to undermine public confidence in Health Surveys in order to shore up the defences of the GSGB reflect poorly on those involved and have prompted activists to describe the use of NHS statistics as “a con”. If it is a con, then it appears that both HM Government and HM Opposition are in on it. In last week’s debate the shadow gambling minister, Louie French (Cons, Old Bexley and Sidcup), and the DCMS minister, Stephanie Peacock (Lab, Barnsley South) chose statistics from NHS Health Surveys rather than the GSGB.

Last year, the Gambling Commission wrote to the Betting and Gaming Council (‘BGC’) to ask it to stop referring to Health Survey statistics. It now transpires that it did so on behalf of the activist organisation, Gambling with Lives (‘GwL’). On 2 October 2024, GwL wrote to the Commission to ask whether it would take action against the BGC for continuing to use NHS figures (which have the status of Accredited Official Statistics) in preference to those from the GSGB (which don’t). Eight days later, the Commission did precisely that – copying and pasting the GwL objections into an email to the trade body. It did so despite the fact that the BGC’s actions do not constitute misuse; while turning a blind eye to cases of actual misuse. The regulator will presumably now also take the DCMS and shadow minister to task for the ‘non-crime statistics incident’ of believing the NHS.

The publication of the NHS Adult Psychiatric Morbidity Survey and the GSGB 2024 this summer will put another couple of ‘problem gambling’ figures into the mix; and these will be supplemented next year by the Health Survey for England – unless the Commission intervenes (it has told the Department of Health and Social Care that it wishes to ‘manage’ statistics that compete with its own). The chances of clarity or coherence breaking out any time soon seem slim.

In September 2019 we wrote a blog titled ‘the myth of growth’, using UK data to show that gambling had not grown materially in real terms for twenty years. A lot has changed in five years: online gambling has grown by another 30% and lockdowns have transformed the way people consume entertainment in a lasting way. However, fundamentally nothing has changed: people are spending less on licensed gambling in Great Britain now than they were in FY19. There are a number of important reasons for this which should shape domestic policy and international comparison as well as UK-facing operations management.

The Gambling Commission’s annual industry stats for FY24 (to March) look optically robust. The top five online group operators, for which the Commission publishes monthly revenue each quarter, have continued to lose share as expected, meaning underlying growth was higher. In the more consolidated betting market, top-five (really 4) share loss was 0.7ppts to 86.7%, which meant betting licensees outside the top operators grew by 10% YoY while the top operators grew by just 3%. The difference in gaming was even more pronounced, with 3.0ppts of share lost to 67.5%, meaning gaming operators outside the top five grew by 20% YoY, vs. 4%. While there are some operational reasons for this difference in performance (biggest isn’t always most innovative and at least two of the top five have suffered from self-inflicted problems caused by weak leadership), we continue to believe that the biggest reason for the shift is an uneven regulatory landscape. In our view, the £5 slots limit which is now been brought in will help to level the regulatory landscape down (something many of the top five advocated for on the basis their performance against the black market wasn’t being judged), thereby pushing a material volume of future underlying demand growth into the black market. Stronger-than-visible growth concentrated principally into the gaming long-tail is a double-edged message for future growth and channelling therefore.

UK online growth has accelerated into calendar 2024 (see Financial Update on Q3), in part because of comps but also because of a dangerously misunderstood phenomenon: the lag effect of money printing and inflation. It has been a while since a gambling operator tried to blame a ‘cost of living crisis’ on poor operational performance. The real reason for the 2022 economic shock (which had a negligible impact on gambling) was a hangover from frantic state money printing during lockdowns; these have now washed through, but average salaries in 2023 were 15% higher than in 2019 (note the gambling sector is not 15% bigger), broadly based salary increases are still coming through (c. +5%), while the government continues to use deficit spending to fund the public sector, adding to inflation risk going forward. When the economy was sclerotic, but inflation was consistently c. 2%, then 4% growth meant something; with inflation likely to remain volatile regardless of central bank predictions, absolute growth is far less relevant than relative growth. Largely due to wage increases and inflation, we expect high single digit growth for online gambling in the UK subject to black market leakage, but we expect a relative decline in gambling revenue – with landbased gambling bearing the brunt.

FY23-4 marked a period of optical landbased recovery, with all landbased sectors except the struggling National Lottery in growth. However, while landbased sectors in total added a net £63m to Britain’s gambling industry (excluding pub gaming machines, likely down), online added £471m, or 88% of all growth. This is a clear case of channel shift at work in ‘frog boiling’ form: landbased sectors are relieved to see some absolute growth but are losing relative market share. Again, inflation is an enemy in disguse – revenue goes up as businesses become less relevant and more fragile.

However, three long-term consumer demand trends are much more sticky than channel shift.

The first is that the National Lottery has failed to maintain early levels of consumer interests (note, now under new ownership). This has been compensated for in part by the strong rise of the Charity Lottery sector, but this is a complementary rather than competitive product: nothing can replace a well-run lottery in terms of mass market customer engagement.

Second, is the slow rise of slots content as the digital experience proved more flexible and increasingly more appealing than Britain’s stunted landbased offer. The new online stake restrictions are likely stymie and probably reverse this trend, in our view.

Third, is the consistency of betting: football has overtaken horseracing in absolute revenue (by only 15% in FY24 after a generation of predicted doom for racing from betting commentators who preferred opinion to evidence), but betting maintains remarkably consistent in terms of revenue mix over twenty-five years despite all the hype over growth. The relative growth in slots has therefore partially mitigated the relative decline of National Lottery revenue to keep gambling expenditure as a proportion of Household Disposable Income relatively stable at c. 1% over 25 years (note, FY9 was low because of the implementation of the Smoking Ban, the loss of S16/21 machines, and the onset of a global recession). However, an underlying decline can be detected and if the National Lottery is not turned around then it is likely to become more visible, in our view.For all the hype about a changing landscape, very little is changing in terms of underlying consumer behaviour other than channel shift. British consumers are, if anything, gambling less, albeit with revenue concentrated in a smaller number of participants.

The growth visible in the FY24 industry stats offers more to be concerned about than relief for a recently battered industry. For the British gambling industry to have a future that is not a story of increasingly pronounced relative decline temporarily disguised by inflation, it needs to achieve ‘just’ two things, in our view: ensure the legislative and regulatory framework keeps high value players in the licensed ecosystem; the opposite is currently being achieved (note, London has already largely lost a c. £150-300m annual high roller casino segment taxed at a marginal rate of 50% – sufficiently specialist to disappear largely un-noticed) create products that have genuine mass-market appeal (the Charity Lottery sector is the unsung standout success story here) These two drivers of industry sustainability sound simple, but they are proving dangerously elusive to deliver.

UK: RET policy – money, money, money: why the levy is far from funny “What operators rightly hate being told is that they ought to be contributing more than they are to RG programs without being told what they are actually paying for. They then readily form the suspicion that most of their money is spent on the cost of employing an army of hostile public and quasi-public officials. These officials are then perceived as having as their primary concern not the alleviation of suffering but the retention or expansion of their own jobs. This in turn, can be suspected of leading to the proliferation of regulations that have little or no empirical basis.” Professor Peter Collins, 2003

The decision to impoae a safer gambling levy on licensed gambling operators in Britian is by far the most ill-considered of the policies contained within the previous British Government’s white paper on regulatory reform. It is also likely to be the most significant in the longer term, with far-reaching consequences for the functioning of the gambling market, harm prevention and policy coherence. In this article, we set out why we believe the levy is bad policy, what its outcomes are likely to be and how some of its worst consequences might be mitigated. Why the levy is bad policy The imposition of the ‘safer gambling’ levy has been dressed up by proponents as self-evident. After all, what could be more reasonable than requiring gambling businesses to fund the treatment of people suffering gambling disorder as well as work to better understand harm and to prevent its occurrence? The polluter, as the trope goes, should pay.

The problem is that is not how our society works. In the normal world, businesses pay taxes at rates set by HM Treasury, which are used to fund public services, including healthcare, research and education. Charities, community groups, and private businesses address gaps in what the state is prepared to fund. The safer gambling levy breaks this model by requiring treatment and other costs to be funded directly from the expenditures of gambling consumers. In so doing, it sets a precedent for levies to be funded against general retail businesses (to recover costs from compulsive buying behaviour), internet providers (internet use disorder), coffee shops and teahouses (caffeine use disorder), pubs and bars (alcohol use disorder), and restaurants (obesity) among others. Followed to its logical conclusion, it proposes a healthcare system paid for by citizens according to their lifestyle choices. There is a dark and unsettling logic to this if applied consistently – but no obvious justification for its imposition on gambling consumers alone.

Combined with the draft guidelines of the National Institute for Health and Care Excellence, the levy will make treatment providers dependent upon the NHS through the stipulation that they may not seek funding or engage with gambling businesses – effectively penalising those organisations that support the current regulations. One consequence of this model is that – contrary to the spin – the levy increases the dependence of treatment and harm prevention providers on the industry (as a number of public health figures have already observed). In replacing a voluntary system of funding with a tax, the government will tie financing to industry revenues. If consumer spending with licensed operators reduces, so will funding. Organizations lobbying for tighter restrictions on gambling consumers (or higher taxes on operators) will do so in the knowledge that new measures may negatively impact their own finances. The Department for Culture, Media and Sport has forecast a net market contraction of 8.2% as a result of its white paper reforms but this is speculative, and the impact could well be greater (particularly if modernising reforms for landbased operators are delayed). There is a very good chance that the levy brings in less than expected, which would be a major problem if the levy was underpinned by an actual budget or assessment of need.

The levy has been justified by reference to two factors: concerns over the perception of research independence under current arrangements (regardless of whether those perceptions are grounded in fact)the fact that some operators have contributed derisory amounts under the voluntary system The first suggests that government policy is now dictated by perception (which is in turn influenced by lobbying) rather than actual evidence. The second is a red herring – no gambling business of any scale has been guilty of under-funding; and the parsimony of the few is poor justification for the creation of a new tax, although it does justify targeted intervention.

The levy is also likely to be wasteful. HM Revenue and Customs already collects c. £3.5bn in specific gambling duties (in addition to general taxes less Output VAT) from the gambling industry, under direction from HM Treasury. The levy, however, envisages the establishment of an entirely new tax system, designed to collect roughly £100m under a non-fiscal authority, overseen by a levy board. While a Levy Board works well in racing, it is independently supervised with formal betting input (a board seat) and levy collected pays for clearly defined common interest objectives, neither of which apply to the safer gambling levy (although they could). Without these governance guard rails, the potential for waste, error and fraud is enormous, in our view.

The suggestion that the levy Is ‘smart’ appears to be Ir of those Orwellian conceits that has come into vogue in recent years (such as the idea recently expressed in the Lancet that state control is freedom). The logic for determining who pays what – including the exemption of the National Lottery – appears non-existent beyond the results of a sector and product popularity contest among the levy’s engineers. The application of a 1.1% rate to online gambling is justified by the idea that: i) it is associated with higher rates of ‘problem gambling’; and ii) remote operators have lower operating costs. The first is solely true of online gaming and is not true for betting – the ‘problem gambling’ rate for online sports bettors in the most recent Health Survey for England was just 1.2% (albeit it is dangerous to leap to causality given that PG rates are principally set by a product’s popularity). The second is true for some remote operators some of the time – but not for the many others: plenty of landbased businesses have higher margins than plenty of online businesses and the channel has little to do with the outcome. More generally, the suggestion that efficiency should be penalised hardly fits with the Government’s growth agenda. There is a reason why tax policy is generally set by finance ministries and not by regulators. Ironically, based on the premise that online gambling operators are able to pay more because of higher margins, they should be able to offset any margin-reducing tax increases with a reduced Levy rate, though we doubt the logic will be applied so robustly.

The levy is not so much smart as unfair. To provide one example, operators of gaming machines in bingo clubs and arcades are required to pay; but pubs and social clubs providing precisely the same machines are not. Further, the way that the Government has presented the tax is misleading because it is levied on suppliers (at 1.1%) as well as B2C operators (at between 0.1% and 1.1%). The effective rate of the new tax will therefore be applied inconsistently and at rates higher than claimed since we do not believe a recoverability mechanism (ie, the way VAT works outside the gambling sector) has been proposed – and it would make no sense if it did since gambling suppliers exist to serve gambling customers, who are being taxed through gambling operators. There is an additional irony that this highly complex levy, with multiple and arbitrary rates across different gambling products and channels, comes as the government simultaneously seeks to copy another of the previous government’s soundbite-driven schemes, since it will: consult next year on proposals to bring remote gambling (meaning gambling offered over the internet, telephone, TV and radio) into a single tax, rather than taxing it through a three-tax structure. This will aim to simplify, future-proof and close loopholes in the system. Perhaps someone needs to tune the governments’ wireless.

What can we expect next? It has been claimed that the ‘safer gambling’ levy will result in greater resources and more certainty for harm prevention services, which would be a good thing. It will probably (depending on events) bring in more money than under the voluntary system; but that is not the same thing. For one thing, it will involve the creation of new administrative bureaucracy for which no published budget exists (a major lacuna) and, given the way that the state spends money, is unlikely to be either modest or well governed.

Half of the funds left over after as yet unknown administrative costs will be allocated to the perennially over-stretched National Health Service, which will almost certainly prioritise its own services over the requirements of the Third Sector. The charities, who have in some cases been effectively and diligently providing treatment to people with gambling disorder for more than half-a-century, will now be required to bid for the funds that were previously theirs. Several harm prevention organizations have already started to shut down programmes (including training for licensees) and making members of staff redundant (up to 150, if reports are correct). Made dependent on the state, treatment providers may find that they are required to fall in line with radical public health ideologies, such as the belief that adults bear no responsibility for their actions and harm is solely the result of exposure to ‘addictive products’. This denial of human agency breaches a core tenet of psychotherapy and has the potential to cause enormous damage to vulnerable people by institutionalising victimhood.

A further 30% of net funds will be allocated to the conveniently vague domain of ‘harm prevention’. Rumour suggests that the commissioner will be either GambleAware or OHID. The former has already called for mandatory health messages on all gambling advertisements (including for the National Lottery and horseracing); while the latter has manufactured suicide statistics and proposed ‘plain packaging’ (no colours, logos or images) for all gambling products. GambleAware may be slightly less illiberal than OHID, but both have trouble distinguishing between harmful gambling and gambling – a blind spot that ultimately leads to long-term prohibition via a medium-term funding bonanza. We can only imagine what they might get up to with up to c. £30m a year.

The final 20% is allocated to research under UK Research and Innovation (‘UKRI’). It is to be hoped that UKRI demonstrates greater scientific rigour and moral neutrality in commissioning research than the Gambling Commission, GambleAware, or OHID. The risk, however, is that it becomes a slush fund for anti-gambling activism that will be used not just in Britain but internationally to campaign for the prohibition of gambling once all the funding that can be extracted has been. In recent years, a profusion of clearly agenda-driven journal papers and reports of low academic quality have been published – often as a consequence of Gambling Commission or government funding – alongside a very small number of high-quality studies. There is a risk that the levy will be used to fuel a propaganda engine for an international anti-gambling movement. The reason why activists have prioritised the levy above all other matters is because they know just how large the prize is – up to £20m per annum.

For all the high-minded rhetoric, the levy seems destined to result in disruption to treatment services, increased stigmatisation of gambling as a legitimate adult pastime, and the production of misinformation on an industrial scale which politicians and bureaucrats seek to lack the discipline or inclination to critically assess.

What should be done now? The safer gambling levy may be bad policy, but it is now policy, and it will come into force next year. The question is therefore what ought to be done by licensees and others. We make three suggestions: Governance – there is a good chance that money raised by the levy will be used inefficiently, unscientifically and inappropriately. The process for how funds are allocated and assessed therefore requires close public attention. Scrutiny should be applied to the levy’s governance arrangements and the process of evaluation in 2030. Given what has gone before, it would be naive to trust those responsible to mark their own homework Continued support – a large number of harm prevention organisations now face uncertain futures. It would be a mistake, in our view, for operators to cease their support for charities and other harm prevention organizations once the levy kicks in even at the cost of ‘paying twice’. Several important programmes now face defunding (in addition to those that have already fallen by the wayside); and operators need insights from these groups in order to inform their own ‘safer gambling’ initiatives – for the sake of disordered gamblers and the sustainability of effective treatment, a distinction must be made between the sunk cost of a pollicised levy and productive expenditure on mitigating the harms that the licensed gambling sector does cause or exacerbate Critical analysis – the levy is likely to result in an expansion of anti-gambling activism, particularly in the domain of ‘research’, which will reach into other jurisdictions. To date, the licensed gambling industry in Britain and other jurisdictions has done an extremely poor job of assessing and (where appropriate) rebutting bad science. It is critical that it develops both the technical capability to scrutinise research and the willingness to call out misinformation (including misinformation which seems to support the industry). There is a good case to be made for building this capability on an internation basis.Ironically, the new levy is at least in part the unwitting handiwork of some of the largest licensees in Britain’s gambling industry whose lobbying made the policy almost inevitable. The Betting and Gaming Council’s endorsement of the policy was unfathomable to us at the time and continues to be so; it makes a lobbyist’s job much easier in the short-term but the industry’s job far harder in the long-term. There is a lesson here which the industry should now be able to perceive – policymaking is difficult in this space; and the pursuit of easy fixes is liable to end in disaster. Unfortunately, the government may have to wait a little longer before it arrives at this epiphany.

Regulus partners

Disclaimer; The analysis provided in this report represents the opinions of the authors. Any assessment of trends and change is necessarily subjective. The information and opinions provided herein are not intended to provide legal, accounting, investment or policy advice, nor should they be used as a forecast. Regulus Partners may act, or have acted, for any of the companies and other stakeholders mentioned in this report.

UK: ‘We don’t need no thought control’ – why the Gambling Commission should leave NHS stats alone

In recent years, the Gambling Commission has been on the receiving end of criticism from all sides of the so-called gambling debate. Last year, the MP, Sir Philip Davies declared that the regulator was “out of control”, while the Social Market Foundation has described it as “not fit for purpose”. The Commission has not publicly endorsed either of these views – or advertised them on its website – presumably because it considers them to be untrue as well as unflattering. Last month, however, the Betting and Gaming Council (‘BGC’) was asked by the Commission to make claims about the prevalence of gambling harms which are probably false – and to publish them on its website.

In an email recently released under the Freedom of Information Act, the Commission wrote:

“We’ve been keeping an eye on use of GSGB [Gambling Survey for Great Britain] data and use of figures as the official statistic. We’ve noticed that BGC still refers to previous stats, it’s not a misuse of stat issue but we’d be keen for you to start using the official figure moving forwards.”

This invitation was politely declined by the BGC on the grounds that it has greater confidence in NHS statistics (which are accredited by the UK Statistics Authority) than in the Commission’s (which are not). The BGC is similarly unlikely to profess that its members are (to borrow from Blackadder) ‘head over heels in love with Satan and all his little wizards’; but the Commission can always try.

The regulator’s entreaties should be considered in the light of the following circumstances: i) the balance of evidence indicates that the GSGB substantially overstates levels of gambling and gambling harm in Britain ii) the Gambling Commission knows this iii) in asking the BGC to go along with the charade, the Commission is acting, at best, inconsistently iv) the GSGB is already being used (and misused) by activists, seeking to reopen the Government’s Gambling Act Review.

We examine each of these points in turn.

1. The balance of evidence The GSGB may be the new source of official statistics, but this does not mean it provides a reliable picture of gambling prevalence in Britain. To believe that it does, it is necessary to subscribe to the following: i. Every single official statistic on gambling and harmful gambling produced over the last 17 years – by the National Health Service (‘NHS’), the Department for Culture, Media and Sport and the Gambling Commission itself – has been substantially wrong ii. The NHS has serially misreported the prevalence of health disorders in general – and continues to do so iii. Audited data on actual customer numbers using licensed operators is incorrect (or there is a massive black market that failed to show up in previous studies and of which the Commission was previously unaware) iv. The opinion of the independent review (conducted by Professor Sturgis of the London School of Economics) that the GSGB may substantially overstate true levels of gambling and gambling harm is misguided

To believe that all these things are true (and to cajole others into professing the same) requires more than blind faith and a sheriff’s badge. Tellingly, the Gambling Commission does not have very much confidence in the GSGB itself; and has issued guidance that key results should be used “with some caution” or not at all.

2. Withholding evidence (again) The Gambling Commission’s defence of the GSGB has largely consisted of attacks on NHS statistics, claiming that they have under-reported rates of ‘problem gambling’. While scrutiny is important, undermining accredited official statistics on health is a step not to be taken lightly. Some sort of evidence is required. For this, the Commission has relied upon a 2022 study which claimed social desirability response bias (ie, the fact that people sometimes answer survey questions in what they consider to be an acceptable rather than accurate fashion) caused under-reporting of ‘problem gambling’ in NHS surveys. This ‘evidence’ was thoroughly debunked by Professor Sturgis as part of his independent review – but for reasons known only to the Commission, the analysis was suppressed. It required a Freedom of Information Act request to secure the release of the information. This is not the first time that the Commission has prevented publication of critical evidence – having previously withheld survey data on customer opposition to affordability checks. Disclosures also reveal the Commission was warned by its lead adviser, Professor Heather Wardle, that social desirability response bias was likely to be a “marginal factor” in explaining differences between the GSGB and Health Surveys (and that the dominant factor of topic salience bias resulted in over-reporting in the GSGB).

3. Two-tier thought policing? In recent years, various parties have taken highly selective approaches to the use of ‘problem gambling’ statistics – often ignoring official estimates in favour of more convenient alternatives. Last year, the National Institute for Economic and Social Research did so in a report funded by a Gambling Commission settlement – using a rate two or three times higher than the official statistic. There is no suggestion that the Commission objected to this. In public consultations, the Commission itself relied on ‘problem gambling’ prevalence rates from the 2018 Health Survey for England rather than lower figures from the 2021 edition (ie, the official statistics at that time). In a speech in Rome last month, the chief executive of the Commission, Andrew Rhodes criticised those who wished to “turn the clock back” to previous official statistics, and in the very same speech cited participation estimates from ‘previous official statistics’.

4. The weaponisation of research The importance of all of this has been amply demonstrated in recent weeks. Both the Institute for Public Policy Research and the Social Market Foundation cited the GSGB’s inflated rates of ‘problem gambling’ in support of demands for ruinous and self-defeating tax rates (as high as 66% of revenue); while GambleAware has used the survey findings to call for tobacco-style health warnings to be slapped on all betting and gaming adverts (including those for the National Lottery). The Commission appears, therefore, to be encouraging the use of inaccurate statistics on gambling harms in the knowledge that they will be used in support of an anti-gambling agenda.

The Chancellor would be wise not to kill one of Britain’s few remaining golden goose industries

“I know we cannot tax and spend our way to prosperity.”

These were the words of Chancellor Rachel Reeves to the business community ahead of this week’s International Investment Summit. This was an event she championed as a way to try and promote growth.

I cannot agree more with those sentiments. But taxing business to the point of oblivion will hobble growth, not deliver it.

The Betting and Gaming Council (BGC) members I represent annually generate £6.8bn into the economy in gross value added, according to figures compiled by EY. They raise a further £4bn in tax for the Treasury, while supporting 109,000 jobs.

This is a huge business, with around 22.5m adults in the UK enjoying a bet each month. The overwhelming majority of them do so safely and responsibly. It is part of our British heritage and culture as well as a bastion of the leisure and entertainment sector. It has made our members – companies such as Flutter, Entain, evoke, Bally’s and bet365 – global leaders, generating billions for the UK.

Crucially, these are not just London-centric operations. Our members have headquarters in Stoke-on-Trent, Newcastle-under-Lyme and, as the Chancellor rightly recognised, in her very own city of Leeds.

We have always been clear that proportionate regulations and a stable tax regime are the only foundations which can deliver on the Chancellor’s ambitions. In order to continue to invest and grow, our members need confidence and stability. Both have been in short supply in recent years.

When the previous government finally published the Gambling Act Review white paper, the BGC welcomed the balanced and proportionate measures it contained.

However, there is no sugar-coating the reality: it will cost our sector well over £1bn a year in lost revenues once all the measures are implemented. It includes a new tax in the form of a statutory levy of £100m a year to fund research, prevention and treatment services to tackle problem gambling – an issue the NHS’s Health Survey for England has confirmed affects just 0.4pc of the adult population.

As we wrestle with those seismic changes, the last thing we need is a further tax rise being demanded by anti-gambling campaigners. They gleefully claim that increasing taxes as high as 50pc will raise billions for the Treasury, while having zero impact on businesses, jobs or key sports we fund such as horse racing. It’s fantasy economics and they know it. Any tax rises now, of any scale, will land a hammer blow to one of the Chancellor’s few growth sectors.

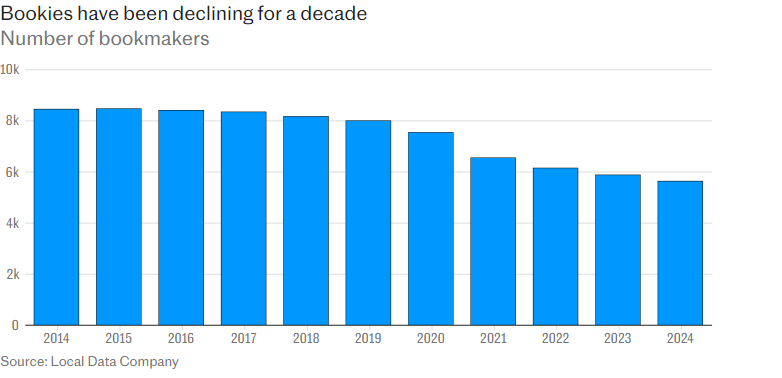

Contrary to the cries of campaigners, betting and gaming is not a soft target. Putting up taxes or imposing draconian regulations does huge damage to businesses. For example, recent regulatory changes directly contributed to 2,485 bookmakers closing since 2019 – a 28pc reduction with the loss of over 10,000 jobs and the business rates they generated.

You cannot put “rocket boosters” under sectors such as ours, as Liz Kendall, the Secretary for Work and Pensions, said at the Investment Summit, while also slamming the brakes on our industry with tax hikes and changes which drive customers away.

The pain is also not restricted to our members, it directly hurts sport.

Horse racing is the most obvious. The affordability checks – a construct totally unique to betting – has hastened double-digit percentage declines in betting turnover, effectively making it close to a loss-making product for some of our biggest members.

Football, especially in the lower leagues as well as in rugby league – a sport much lauded by Lisa Nandy, the Culture and Sport Secretary – along with other working-class sports, such as snooker, darts and boxing, rely on the income betting delivers. Hit betting and you will hit sport, from the grassroots to the elite level.

There is another issue blithely ignored by armchair economists, the growing threat of the unsafe, unregulated black market. A recent study found 1.5m Britons stake up to £4.3bn on this gambling black market. These operators offer deals too good to be true, circumventing the crucial player protection tools standard across BGC members. They also don’t pay tax, don’t create UK jobs and don’t support sport.

Rachel Reeves is right to go for growth. So it would make no sense whatsoever in the Budget to over-tax a gambling industry which has been hit hard by the Government in recent years. We want to play our part in investing and helping to grow the economy. The Chancellor would be wise not to kill the goose that is already laying the golden eggs.

More than a decade ago, I sat down to lunch with the eminently amiable Simon Bazelgette. At the time one of the decision makers in the s[port, as leader of Jockey Club Racecourses. My online business was fledgling, years behind 365, I spent my time with reasonable prominence on racetracks with good pitches, and laying bets others would not. My interest lay in attendances at racetracks

He told me of their plans to bolster what was a successful sport, with concerts. The unspoken master plan involved a lake of beer.

For a while, the plan seemed to work. Top acts were booked, and given this was all new territory, their rates were affordable. Racetrack sales grew, alcohol seemed a happy marriage as Bazelgette’s argument was tracks needed to ‘evolve’ to become more of a leisure day out, than a sport. Not that he associated alcohol sales in conversation

Over the years, the top acts, other than legacy performers well past their sell by, like Tom Jones and Rod Stewart, raised their rates, and the maths started to bite. A clear example was Epsom (I might refer to this old Dame a few times) which booked concerts by acts most regular attendees of tracks had never heard of, and put on six class 6 races for pocket money. Yes, you heard that right, whilst claiming the practice was to encourage fans into the sport, they often afforded exceptionally poor racing. Being Epsom, some of the field sizes were miserable. But the track was busier than ever, and profitable for a change. All seemed good in the world of racing. The formula was taken up across the sport

There were downsides, but these seemed trivial when a night meeting at HQ could draw in 15,000, and beer sales were impressive. As were the vital corporate boxes. For example what were the views of their older core membership to seeing the racing programme often dumbed down? Did they relish sharing their sport with large groups of young men and women, too drunk to stand by the third race? A category of spenders were sold members enclosure tickets.

Bazelgette told me ‘racing entrance charges are favourable against football’

But Simon should know, as every racetrack should, racing is 90% downtime – filling empty space rather than a seat, and often features a rather poor betting only product. Football is 100% action. Even cricket beats Racing comfortably in said regard. So if your leisure product is simply beer- it better be a superb environment to keep people entertained for 4 hours!

Worst of all, the brigades of sockless wonders brought aggression to the sport. Fights at venues like Epsom, Ascot and Newmarket were constant. I witnessed many of them personally, as I am sure we all have. The regulator of the sport, the BHA, looked on impassively. It never sanctioned a single racetrack for their failures to deliver a safe, fight free environment for all. One would have imagined social responsibility to be the domain of the regulator, but fat chance when BHA executives are selected by racetracks

Drugs were rife too, with queues for cubicles at toilets on a biblical scale. Children were actively discouraged from attending at tracks like Epsom by pricing policies of full adult rate for a child. It was as cynical, as it was short sighted. A decision without question because the track executive considered the environment as simply too toxic for the young. And i wouldn’t disagree! I watched huge enterprises like Ascot, the Kings racetrack, throw its effluence casually out onto the local community at 6 o clock, without mind of the consequences, nor the effect on the local community

This was the business plan for racetracks, but not the sport. Of course it all came to a grinding halt when the rates for bands became untenable. Although the beer sales remained. At some formerly impressive tracks I’ve seen beer machines spring up. I mean, I ask you what socially responsible business does that? What kind of culture are you trying to create when a pint of beer is sold by a machine, and overpriced champagne is served in a plastic beaker? Aren’t you trying to create a civilised, cultured environment? Who is governing who gets a drink, or when is enough? Perhaps a student attendant at best. Coffee, the highly popular staple diet of high streets across the country, has never been taken up properly by track execs. It can take several minutes to make a coffee, just seconds to pull a pint. It boils down to money over service standards

Finally, as far as racetracks are concerned, there’s the cynical pricing practices. Charging the maximum for meetings which appeal only to betting. Racegoers finding bars and restaurants closed. How some tracks can charge £120 for a bottle of champagne – served in a plastic cup, on cheap tables, whilst the same bottle in York costs half that amount? Car parking charges are excessive. No track is exempt from criticism here. The food on racetracks – outside the private boxes is notorious. What would tracks do without vans serving chips? There used to be an excellent sweetie van at Ascot, run by people who have provided such a service for years at many racetracks. It’s been replaced by a dismal track equivalence. Why? Because new management have decided it to be more profitable in house. The service angle has been shelved in importance. The same people no longer serve Goodwood. Why? Because they can’t afford the rates. Now noone offers that essential service, with such panache

Tracks have gone cashless, often refusing to countenance any cash sales, from punters who arrive at the track with cash only for bookies, and who, when they win, cannot spend it at the venue. This kind of management is child-like. The current estimate of cash circulating in society is 82 billion. And the tracks have decided they don’t want any of it? It is an astonishing fail. Me? I’d take green shield stamps..

Cash is legal tender, and if you’re not going to take it, make it clear when people buy a ticket that you refuse to accept the paper.

In the simplest terms possible, racetrack executives have markedly contributed to their own downfall. With cynical pricing practices and quite often severely run down racetracks, lacking appreciable investment

One final point, I think racetracks appear to have missed. They’ve become almost universally unpopular with their patrons. Few letters appear which glorify the experience. Few articles laud racetracks for service, value or customer experience. And noone likes their attitudes to social responsibility. In said regard they rival ‘big corp’ bookmakers for popularity. With few exceptions.

For two decades almost, I have railed against the practice of breeding in the sport. Let me give a topical example, – City Of Troy. A rather in an out character, with sour performances in the Eclipse and the 2000gns. In between which, on going days, he can be endlessly impressive. The general public, and more importantly the racing crowd, have started to associate with this new star. Bolstered by plaudits ‘best i have ever trained’ from the very likeable, and hard working Aiden O Brien. He could sell me windows any day, training is just his day job. They were even afforded a racetrack gallop at Southwell, the performance enhancing element for which was unclear, since its characteristics against Del Mar, California, appeared only to be the running rail. I mean if you want a racetrack gallop – and you live in Ireland- Dundalk is just up the road.

What it was, however, was a giant sales pitch. City ‘raced’ against some of the worst horses in the AOB yard, and duly ran away. A visual display. A clever marketing ploy to up the price of breeding to those interested. Given it was covered by many racing journalists and television, it was an enterprising move, rewarded with coverage far beyond its worth

I think we all know if City Of Troy wins in Del Mar, that we will hear he is to be retired. At best, this performer won’t make it on a racetrack to 5 years. And this is the true cancer in the sport. Horses carted off to stud far too early in their careers. It is indeed a rarity for anything winning France’s Arc to continue on. The call of a lucrative career making other racehorses far too compelling. Tattersalls book 1 registered a staggering 134 million in sales this October. An absurd figure for an auction notorious for delivering on failure for the majority of purchases. Could there be a bigger bubble?

Troy will yield an impressive purse at stud, far more gained in a month than could in a career as an actual race horse, entertaining the general public. And this, my friends, is where the real money in racing is. Not actually racing.

Breeders will argue, and some may agree, that his progeny will entertain racing fans for a decade. That argument, however, falls entirely flat when you look at what draws in fans to other sports. Lionel Messi has been entertaining football fans for more than a decade. Joe Montana did the same in the NFL, and Johnny Sexton wowed rugby fans until his body gave out. Racing farms its best out to barns in a naked exercise in cash creation

This is what brings people to sport. In tangent with an ability to adapt. Cricket is the best example of that, introducing twenty twenty slogs, and 50 over games to afford fans the one day bash they craved. They still keep the 5 day borefest of course, for the aficionados, but attendances are modest. The NFL routinely changes its laws and rules, ensuring every team across the nation has a chance at the Superbowl. Dallas used to dominate, now they’re a mid table performer. The system of capping and drafts arresting billionaires from buying their way to enduring success

And whilst other sports have been improving their offering? The BHA have been watering down its fare. Banning hard pressed jockeys for obvious errors, a clear violation of their human rights. Low sun meriting bumper races. A massive dumbing down of National Hunt fences, the leading example of this would be the sport’s shop window. The Grand National

Now I do understand that for a decade animal rights campaigners have hung around Aintree, peddling their views. They should be easy to counter, over 90 percent of the animals they ‘save’ are euthanized! Any attempt to ban racing would amount to the biggest cull in the horse ever undertaken, and critically the RSPCA sees no issue with horse care. In the last few years, Aintree has experienced more horse deaths in the National than in the entire decade of the 60’s. It seems to me that speed kills with far more effectiveness than the height or stiffness at fences. Look at Cheltenham’s 3rd last, now removed. It was rightly accepted that with the downhill nature of the fence, the tiring horse being asked for extra effort, led to fatalities. Nick Rust decided it was all about height, and the latest industry patsy, Julie Harrington, without doubt the most ineffectual leader the sport has ever engaged, it was also about how many actually took part.

The clear and indisputable result was a race where over 4.5 miles, not a single horse fell. Not one. And in previous years I watched the same farce being played out with the number of finishers determined by those who pulled up.

The shop window has seen a huge decline, despite an attractive time slot, in the number of people watching the race. A nod to animal rights- has become the sports headstone, indeed they’ve created a monster. Hearts in their mouths every year-and with the inevitable spectre of future horse fatalities, will require another response. That’s how appeasement works.

Some folk in racing are waking up to the third issue. Trainers. The sport is ruled by a miniscule posse of top trainers. The aforementioned O’Brien, dominates the flat, and has become so powerful he can openly flout the rules of the sport, employing team tactics for example, to ensure his stars have the ideal pace and running line. Horses with best form at 7 furlongs sent out in Irish Derbys to provide the best environment for other horses in the stable. O’Brien may be breaking the rules, but he’s not doing anything wrong. Why? Because it is condoned by the authorities, and therefore he has cleverly made it legal.

The Irish racing regulator, Horse Racing Ireland came up with a novel plan to limit just 60 races in its programme to trainers who had fewer than 50 Irish Hunt winners. There were endless good reasons for such a plan, if you want to reduce the power of Mullins and Elliott, and to a lesser extent the likes of De Bromhead and Cromwell, from winning everything meaningful. It is precisely why other sports employ salary caps. Such dominance in any sport is deeply unhealthy, and pressurises small trainers out of business. Mullins, for example, can withdraw his horses from a particular meeting and the bottom drops out of all interest. These 4 trainers were rumoured to be considering legal action, to protect their dominance, which merely serves to illustrate how self serving they are

Add that to the endlessly ruinous practices of other horse husbanders, like Nicky Henderson, withdrawing top stars from races at the eleventh hour, with a range of spurious excuses. Without due care for those who have bought a ticket. It is about Seven Barrows, rather than the National Hunt, and I’m afraid that’s as unacceptable as Manchester City deciding not to play its best players, because the opposition might be a bit stiff

Both the BHA, and Horse Racing Ireland have afforded trainers luxuriant opportunities to gain coveted black type. This has several major benefits to owners, breeders, trainers – but not the tracks. Naturally a row of often cheaply gained graded wins raises the profile, price and stud fees, and racetracks see offering graded events as important to attendance. Such has become somewhat of a millstone. Racing channels, pundits, hacks can all laud the performances of horses like Constitution Hill, but they are gained at the expense of competitive racing. I struggle to understand the eye watering fawning over such performances, when those who could make the race of merit to fans and television are boxed up and sent elsewhere. Ultimately, however, the practice has hit the sport hard, with a marked decline in attendance. Aficionados can glorify group races like the Eclipse, Goodwood Cup or Champion Hurdle – but they remain utterly meaningless in terms of competitive fare, and for the betting public at racetracks? An irrelevance

Racing is not helped by its inward looking approach. Too many decisions involve self interest, the views of John Gosden, the tracks themselves, or the breeding community. Racing’s hierarchy is drawn from the sport almost exclusively and there are precious few new ideas. Attempts at change are derided as unnecessary – or even face legal challenge. Either that culture changes or the next generation could be looking at a severely diminished sport.

Affordability checks in the gambling medium can only negatively impact racing coffers. I understand the reaction of the tracks will be to run to government to renegotiate what they earn from bookmakers. This has always been just so. It is a poor business practice, however, to refuse to accept the sport has declined in interest and competitiveness, and not to care that bookmaker returns in an expensive sport to operate are borderline, and racing’s most important stakeholders – punters, are fast losing interest in betting on the sport. They would rather bet on the slots, according to the latest set of financials from the GC.

Black type should be at a premium. Everything that can be done to increase competitiveness and participation must be addressed. Racetracks need to stop treating the sport as a by product to their publican tendencies. Prices cannot rival football, because racing isn’t as good as football. And the practice of breeding has to be robustly challenged with measures designed to make it a lot more difficult for horses to line up a row of 1s. The sport isn’t about 10 trainers.

Most sports would have woken up to its issues and taken full ownership a long time before now. In simple terms our decision makers view the sport from the corporate box, and show no understanding of why people are voting with their feet elsewhere

When racing was threatened by the prospect of a massive drop in income with the gambling commission’s utterly futile affordability checks on punters, a petition was taken up to get Parliament to debate the matter further. I recall it took nearly two weeks to gain 100,000 signatures. A sport with at least that number of people who depend on it for employment or business struggled to muster support. Why? Because the air of snobbish indifference to those who bet on the product came to the fore. The idea what is good for a bookmaker as good for the sport, not an ideal they care to support. Which highlighted a patent lack of understanding how the sport is financed by many. I have had many conversations with people in the sport who simply do not understand how dependent they are on betting! Punters themselves have felt entirely disenfranchised by association with racing. Overcharged when they attend for a very poor sporting product. Treated poorly by big betting corporations, and ignored by the authorities such as the BHA and gambling commission. The latter who actively punishes them for transgressions by major betting giants. Not difficult to see their indifference.

If racing is to get through this crisis, it simply needs a new authority. Which isn’t hired by the sport. Given free rein to sweep through changes. Punish racetracks for social failures and inadequate facilities. Enough of vanity Group 1s like Saturday’s Dewhurst. 5 ran- 2 owners. Weighed in. And the breeders? Well, they are racing’s true enemy. Forcing lesser owners out of association and robbing the sport callously of its stars as juveniles. Think that’s an extremist view? Well, tell me in November where to find City Of Troy.

Regulus partners disassemble an incompetent report, funded by Derek Webb, by Nera Consulting

The 2021 report was written by George Anstey, Soren Christian and Sofia Bittari – three economic illiterates from Nera Consulting (a think tank). It was commissioned by the Peers for Gambling Reform, who were funded by Webb. The 2023 report on New Jersey was written by Soren Christian (again) and Duncan Broadie and was funded by the Campaign for Fairer Gambling. It relied heavily on the bs NIESR report in 2022, which was funded by the Gambling Commission (nuf said!) and led by James Noyes and involved the archangel of anti – Heather Wardle. The NIESR report relied on the entirely unsubstantiated assumption that being economically inactive due to ill-health and WINNING £500 from gambling over two years was a proxy for ‘at risk’ gambling. It’s a case of bs begetting bs.

Derek Webb

Regulus Partners

Introduction

In, May 2021, NERA Economic Consulting published a report on the economic impact of implementation of five proposals for legislative reform contained within the 2020 report of the House of Lords Select Committee on the Gambling Industry

The report was commissioned by the Peers for Gambling Reform (the ‘PGR’), a House of Lords based lobby group

The report was funded by Las Vegas resident, Derek Webb, who is described as a “benefactor of the PGR”

The report’s central claim is that while the implementation of the five reforms would have a substantial impact on Britain’s licensed gambling industry, they would be economically beneficial in terms of increased jobs and taxation at the level of the national economy

This report examines the NERA report in terms of factual accuracy and methodological coherence

The Five Reforms

structural limits on online stake sizes and play speed

affordability checks for online play

the introduction of a Mandatory Levy for gambling operators

the classification of video game loot boxes as gambling

a ban on direct sponsorship by gambling operators.

2

Executive summary I

Our analysis raises a number of concerns with regards to NERA’s report.

The presence of a number of relatively basic factual inaccuracies that reveal a lack of understanding of gambling regulation, problem gambling and Britain’s tax system. As well as betraying a paucity of expertise, these errors have material effects on NERA’s economic impact calculations.

Highly speculative use of data and highly selective use of research to inform modelling

The use of completely untested assumptions to model the effect of legislative interventions – for example the assumption that expenditure by people with gambling problems will switch entirely into shopping, food and drink, the arts and sports in the event of greater online restrictions (and not to unlicensed gambling)

A complete failure to consider counter-factual scenarios (e.g. the possibility that spending might be shifted into activities that result in as much or greater harm such as excessive consumption of alcohol or unhealthy food)

The implausible implication that the remainder of the recommendations in the House of Lords report would have no material economic impact

A failure to consider negative wellbeing impacts on non-problem recreational gamblers and a reduction in consumer surplus

What appears to be a complete lack of interest in whether the reforms sought by the PGR will in fact result in reduced harms

3

Executive summary II

Over and above all the factual and methodological problems with the NERA report, there is also the question about how valid such projections are.

It is not the role of businesses or consumers to create jobs;

It is not the role of Government to intervene in the lives of its citizens in order to channel their spending into sectors with the highest rates of employment and wages

The key issue on gambling reform is how the Government should seek to balance the freedom and enjoyment of citizens against the need to protect them from harm The NERA reports provides no illumination on this question (see opposite)

“If the assessed reforms are effective in reducing harmful gambling activity, some of [the] excess fiscal costs could be reduced. The extent to which this is true depends on:

“How effective the reforms are in reducing harmful gambling activity; and

“The extent to which gambling harm is itself the driver of the excess costs listed in Table 4.8. For instance, individuals with harmful gambling habits may also be more likely to exhibit other characteristics that require greater NHS treatment (e.g. alcoholism), and these other characteristics may not disappear even if the harmful gambling activity does. “We do not consider in this report the extent to which either of the conditions above are true”

4

Overview

We analyse NERA’s report in three areas:

Inputs – the data and research considered by NERA in making its report

Methodology – how NERA produced its estimates of economic impacts

Inconsistencies

5

The inputs I: overview

Much of the information used by NERA in the report is highly speculative, as the authors admit: “Throughout this report, we base our analysis upon the most reliable data available to us. In many cases, especially for data specific to the gambling industry, the data sources are few and far between, and may be based on incomplete samples. Where better data exists in house with gambling operators, this has not been shared with us, and so we cannot rely upon it.”

What the authors do not disclose is the extent to which they attempted to obtain “better data” (e.g. by asking licensed operators to share information).

This is critical – if the data inputs used in the report are unreliable, we must exercise extreme caution when considering any of its outputs. The report is also based upon highly selective and unverified inputs from other sources, as NERA admits: “Information furnished by others, upon which all or portions of this report are based, is believed to be reliable but has not been verified

This is negligent – particularly given the presence of a number of conflicts of interest. Our analysis shows that it was unwise for NERA to assume without checking that the information supplied to them by others is reliable.

In certain instances, the NERA report reveals an absence of basic understanding of gambling regulation, problem gambling and – perhaps most surprising of all – how Britain’s tax system works.

6

The inputs II: basic errors (taxation)

NERA seems to misunderstand the way that value added tax (‘VAT’) works

On page 37, NERA describes the differences between betting and gaming duties and VAT as follows: “The loss in consumption-based tax revenue is due to the difference in how RGD and VAT are assessed. For every £1 a person spends on online gambling, £0.21 is directly recovered as tax revenue, and the gambling operator would additionally pay VAT to its upstream suppliers.

For every £1 a person spends on other activities, they are charged £0.20 in VAT, but a portion of that is used to offset VAT paid by the company to its upstream suppliers. Therefore, a smaller portion of expenditure in other sectors actually makes it to the Exchequer through consumption taxes.”

This description is however incorrect. VAT of 20% is charged on top of expenditure (it is an “added” tax). The passage therefore should have read “For every £1.20 a person spends on other activities, they are charged £0.20 in VAT….”

It is highly surprising that an economic consulting firm should misunderstand the basis for the application of VAT.

The error has a material impact (c.£50m) on NERA’s calculations of revenue lost to the Exchequer.

7

The inputs III: basic errors (duty)

Basic errors

On page 28, NERA describes online gambling taxation as follows: “All online operators must pay 21 per cent RGD on GGY from customers who live in the UK.74 For each £1 reduction in online GGY, therefore, we assume that the industry saves £0.21 in RGD”

This is incorrect – expenditure on online gaming is subject to RGD at 21% but expenditure on online sports betting is subject to General Betting Duty at 15%.

This error has a material impact (c.£40m) on NERA’s estimate of operator cost savings (as well as on projections of lost tax receipts).

Elsewhere in NERA’s report, we also find examples of factual errors in relation to maximum stakes on terrestrial slot machines (p.5) and problem gambling (which is incorrectly conflated with gambling-related harm – p.6 and elsewhere). While these latter mistakes have no bearing on Nera’s calculations, they do betray a lack of expertise and domain knowledge.

8

The inputs IV: unverified claims

The Nera report is based upon a surprisingly thin selection of evidence.

What is more, some of the sources are drawn from parties with clear vested interest – interests that Nera chooses not to declare in its report..

Source Undeclared conflict of interest Noyes, J. & Shepherd, A. (2020) Gambling review and Reform: Towards a new regulatory framework. Social Market Foundation.

Funded by Derek Webb who also funds the PGR and who paid for the Nera report

Cowen, T. & Blond, P. (2018) Online Gambling: Addicted to Addiction. Respublica.

Funded by the Campaign for Fairer Gambling, a lobbying organisation funded by Derek Webb (see above)

Newall, P., Weiss-Cohen, L. Singmann, H., Boyce, W., Walasek, L. & Rockloff, M. (2021) A speed-of-play limit reduces gambling expenditure in an online roulette game.

Philip Newall was expert adviser to the House of Lords Select Committee (and claims to have influenced its report).

Muggleton, N., Parpart, P., Newall, P., Leake, D., Gathergood, J. & Stewart, N. (2021) The association between gambling and financial, social and health outcomes in big financial data. Nature Human Behaviour

Philip Newall was expert adviser to the House of Lords Select Committee (and claims to have influenced its report).

9

The inputs V: unverified claims

Reasons to be cautious

•Source Issues Newall et al. (2021) Unpublished paper with no evidence of peer review and no funding or conflict of interest disclosure. The paper itself is based upon a simulated gambling experiment rather than actual data. Despite these issues, NERA states that “We rely heavily on this research…”

Muggleton et al. (2021) This study of gambling expenditure revealed in bank account data is flawed in a large number of ways – but principally the fact that the researchers looked only at cash outflows and ignored cash inflows. As a consequence the report is based upon a substantial overstatement of expenditure.

Thorley, C., Stirling, A. & Huyn, A. (2016) Cards on the Table: The cost to Government associated with people who are problem gamblers in Great Britain. IPPR.

This report has been criticised by both the Government’s Regulatory Policy Committee and the DCMS.

Cowen & Blond (2018) Produced demonstrably false estimate of the distribution of revenues by PGSI classification (See slide 11) 10

The inputs VI: unverified claims (illustrative example)

An example of how NERA perpetuates claims from misleading research “According to the think tank Respublica and cited in the Committee Report, 24 per cent of the online gambling industry’s profits derived from 0.8 per cent of the UK population it classifies as ‘problem gamblers’. A further 17 per cent comes from the 1.0 per cent of the UK population it classifies as ‘moderate risk gamblers’.’”

The estimate of revenue from problem gamblers cited was first produced by Landsman Economics, an organisation also funded by Derek Webb

The underlying data derives from a PwC report published in 2017 – ‘Remote Gambling – Phase II’

The PwC study deliberately over-sampled problem gamblers: “We can accommodate the above in our approach by our segmentation which deals with product bias, and the fact that we intentionally selected more active gamblers to increase the sample of potential problem gamblers.“ (PwC, 2017, p.18)

The PwC report revealed staking levels by PGSI classification (i.e. problem gambling, moderate risk, low risk) – it provided no information at all on revenue or profit. It is unscientific to assume that share of stake is the same as share of revenue or profit

The House of Lords Select Committee was made aware of this error – but the PGR continues to use it, suggesting perhaps a wilful attempt to mislead

11

The inputs VII: unverified claims (illustrative example)

In a deliberately skewed sample, PwC provided information on mean staking levels and online gambling frequency by PGSI classification

Extrapolation indicated that around 60% of total stakes were bet by 29% of the sample (6% problem gamblers; 23% moderate risk)

Landsman Economics made the baseless assumption that the distribution of stakes in the PwC report was nationally representative and so applied it to the PGSI classification distribution from the combined Health Surveys 2015. This is methodologically unsound. This was presented to show that 41% of stakes were bet by 12% of online gamblers (5% problem gamblers; 7% moderate risk gamblers)

Respublica (Cowen & Blond, 2018) rebadged ‘stakes’ as ‘profit’ and changed the base from online gamblers to all adults (irrespective of whether they had gambled online or gambled at all).

By a series of sleights of hand, ‘60% of stakes from 29% of online gamblers’ magically became ‘41% of profit from 1.8% of the population’.

This is statistically illiterate.

12

Methodology I: spending substitution (i)

NERA fails to provide any evidence for its spending substitution calculations and simply ignores unlicensed market risk

NERA models the economic consequences of the PGR proposals on the assumption that “100 per cent of money not spent on online gambling diverts to” general retail (59%), eating and drinking (28%), creative arts (5%) and entertainment and sports and recreation (8%).

No explanation or evidence is offered in support of these assumptions.

This is problematic given the clear implication from Nera that reductions in gambling expenditure would come from those experiencing harm (which Nera mistakenly conflates with DSM-IV/PGSI ‘problem gambling’).

In other words, NERA seems to make the counter-intuitive assumption that changes to online stakes and speed of play and the imposition of ‘soft’ affordability checks will result in those with gambling problems switching their expenditure to shopping, eating and drinking; while recreational (non-problem) gamblers will continue to gamble.

The idea that someone with a gambling problem will switch from gambling to shopping as a result of stake or speed of play restrictions (and not for example consider continuing to gamble with an unlicensed provider) seems to misunderstand the nature of the disorder.

NERA gives no consideration to the counter-factual possibility that harms may arise from switching expenditure from gambling to – for example – the consumption of alcoholic drinks or HFSS foods. Given that problem gambling is typically a ‘secondary disorder’ and often described as a ‘coping method’, it seems plausible that if expenditure by problem gamblers is diverted to other activities, this may happen in a way that also leads to harm (for example through compulsive buying behaviour, alcohol dependency, obesity or internet use disorder) and imposes costs on society. 13

Methodology II: spending substitution (ii)

NERA appears to assume that the utility of every Pound of expenditure is the same

However, the purpose of the economy is not to supply jobs but rather goods and services which deliver maximum welfare.

If good x is prohibited, and everyone then switches to good y, with expenditure and employment the same, the change is not neutral.

Economic welfare has been lowered because individuals had been signalling from their previous purchases that x gave them more satisfaction than y.

This is the true economic impact.

14

Methodology III: jobs and income tax

NERA provides estimates of growth in employment as a result of consumer expenditure switching from gambling to other activities

It models a net increase of 20,000 to 30,000 new jobs – predominantly in retail and food and drink

Aside from serious concerns regarding the extent to switch consumers would substitute shopping or drinking for gambling, NERA also appears to consider that every incremental Pound of expenditure generates an equal number of new jobs –failing to consider the fact that some industries require relatively high fixed levels of employment and that productivity gains would be expected from large increases in expenditure

In addition, given the huge heterogeneity in terms of average wages and labour intensity attempts to estimate employment and wages based upon historic means is likely to be so imprecise as to be useless

This causes us to question NERA’s estimates of both the numbers of new jobs that would be created and the marginal impact on average earnings (particularly when many of the more highly paid jobs in industry are likely to be found in the fixed employment based)

This suggests that NERA is likely to have substantially overstated estimates of both job creation and income tax generation

While NERA attempts to model the impact of job losses within the gambling industry, it fails to consider impacts on jobs associated with gambling – notably the significant losses from the horseracing industry likely to result from the imposition of affordability checks

15

Methodology IV: impact on licensees

“The gambling industry could lose between £696 million and £974 million as a result of the proposed reforms, but industry profits are most likely higher than this at present.”

Any assessment made at the level of the industry will fail to recognise that different companies are in different positions with respect to profitability (and balance sheet strength). The impact therefore of measures designed to reduce consumer expenditure and increase operating costs will vary significantly between different licensed operators.

Nera seems to assume that the profits generated by the basket of gambling companies from whom it derives its industry profit estimates relate solely to customers and operations in Great Britain whereas they are in fact global.

As a result, NERA fails to explore whether revenue reductions in Great Britain would make that particular market unprofitable (in which case, companies would likely withdraw). This is shown most clearly in its assumption that the licensed online gaming (casino/slots/bingo/poker) market would remain viable following the loss of 76% of its revenue.

In any case, NERA seems to assume that the industry could bear a substantial margin reduction (of the order of 150% to 200% basis points) and still generate value – in other words that the industry as a whole may still be viable so long as it generates some level of profit, even if that profit is lower for example than the cost of capital.

Nera fails to recognise the fact that substantial margin erosion will impact the customer experience and offer a significant advantage to unlicensed operators (who will be in a position to offer far greater rewards and incentives).

16

Inconsistencies I – mandatory levy

NERA considers the imposition of a Mandatory Levy to raise £150m a year from licensed gambling operators.

It assumes that this would be roughly equivalent to 1% of total industry GGY (including National Lottery) and that this would be calculated on a ‘smart levy’ basis (although how such a levy would be constructed is not explained)

Of the funds raised, £20m would be used to fund a new gambling Ombudsman. This is strange as one would normally expect a regulatory body to be funded by licence fees.

The balance of £130m would be collected by HM Treasury. NERA suggests that these funds would be used to support general Government spending rather than being hypothecated to pay for treatment of gambling disorder – or research or education. In other words, it is simply an additional tax rather than a safer gambling levy.

Nera suggests that HM Treasury might subsequently elect to spend £68m to £87m of this £130m on research, education and treatment (‘RET’) – and does not explain what would happen to the balance of £42m to £63m

In assuming that a 1% levy would capture c£150m in payments, Nera neglects to incorporate its own calculations regarding the effect of the PGR reforms (maximum stakes, speed of play and affordability checks) on GGY – reforms that Nera believes may reduce GGY by as much as £2.1bn.

This may in turn have a disproportionately outsized effect if the smart levy is weighted towards online gambling (which, given the PGR’s hostility towards online gambling seems feasible).

NERA fails therefore to consider the ease of collecting £150m via an ad valorem levy while at the same time implementing reforms with the conscious aim of reducing gambling expenditure.

17

Inconsistencies II – sponsorship ban

NERA admits (p.26) that it has modelled no negative impacts on the gambling industry as a consequence of implementing a ban on sports sponsorship. “For revenue effects, we assume that the gambling sector in aggregate will not see a loss in revenue from not being able to advertise their brand via sponsorship of teams.”

Thus NERA assumes a substantial benefit to the licensed gambling industry as a result of cost savings on sponsorship but assumes no loss of revenue.

This invites the obvious question that if sponsorship has no effect on consumer spending (and in particular, spending by problem gamblers), why is it considered necessary to ban it?